FICO 10T vs Classic FICO: What Changes for Your Mortgage in 2026 — Complete Guide

As of April 2026, lenders selling loans to Fannie Mae, Freddie Mac, and FHA can now choose between Classic FICO and VantageScore 4.0, with FICO 10T approved and being phased in. FICO 10T differs from Classic FICO in one critical way: it analyzes 24 months of your credit behavior, not just a snapshot. If your balances have been consistently going down, FICO 10T rewards you. If they have been going up, it penalizes you. The lender you choose in 2026 determines which model evaluates your application — and that choice can affect your approval and rate.

For more than 30 years, one scoring model dominated the U.S. mortgage market: the Classic FICO score. Every conventional loan sold to Fannie Mae or Freddie Mac required it. Every FHA application was evaluated with it. If Classic FICO said no, the answer was no.

That era has ended.

In April 2026, in a joint announcement, the Federal Housing Finance Agency (FHFA) and the Department of Housing and Urban Development (HUD) confirmed that FICO 10T and VantageScore 4.0 are now available to lenders for mortgage underwriting alongside Classic FICO. FHFA Director William J. Pulte called it a “historic move” to introduce competition into the mortgage credit scoring market for the first time in decades.

For millions of Americans planning to buy a home or refinance in 2026, this change raises an urgent question: will the new scoring models help your application or hurt it? This guide answers that question in full — based on official sources from FHFA, Fannie Mae, FICO, and Experian.

What Is FICO 10T?

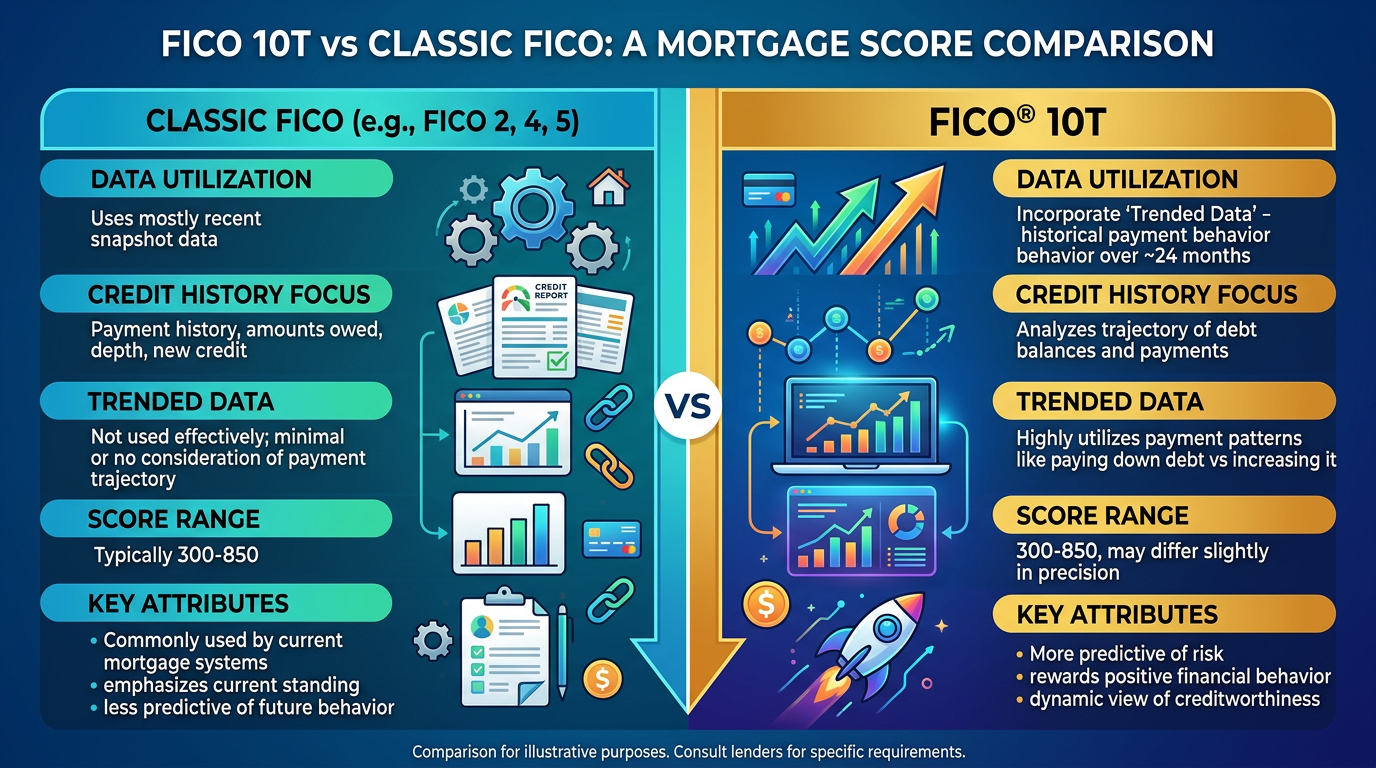

FICO 10T is the tenth generation of the FICO scoring model. The “10” refers to the version number, and the “T” stands for trended data — the feature that makes this model fundamentally different from every FICO version that came before it.

Like all FICO scores, FICO 10T produces a number between 300 and 850. The range is identical to Classic FICO. The factors it considers — payment history, credit utilization, length of credit history, credit mix, and new credit — are the same five factors. What is radically different is how it evaluates those factors.

Classic FICO takes a snapshot. It looks at your credit file as it exists at a single moment in time — the day the score is pulled — and generates your number from that data alone. A 25% utilization rate on your credit cards is a 25% utilization rate. The model does not know, and does not care, whether that 25% represents the lowest it has been in two years or the highest.

FICO 10T asks: is that 25% going up or going down?

It uses the credit bureau’s stored historical data — going back 24 months or more — to determine the direction of your credit behavior. According to myFICO.com, FICO 10T considers “a longer historical time frame (the previous 24 months or longer) of the balance and/or credit limit to get a more refined view of your credit risk.”

Important: FICO 10T Does Not Require New Data

FICO 10T does not require consumers to submit new information. The 24 months of historical data it analyzes is already stored in your credit file at Equifax, Experian, and TransUnion. The credit bureaus maintain your account history for up to 7–10 years. FICO 10T simply uses more of that existing data than Classic FICO does.

What Changed in 2026 — The FHFA Announcement Explained

The path to FICO 10T acceptance in the mortgage market was a long one. Here is the accurate sequence of events leading to where things stand today:

President Trump signed legislation requiring FHFA to establish a process for Fannie Mae and Freddie Mac to validate more advanced credit score models beyond Classic FICO.

After extensive testing by Fannie Mae and Freddie Mac, FHFA formally validated both new scoring models for future use in mortgage underwriting.

FHFA directed Fannie Mae and Freddie Mac to permit lenders to choose between Classic FICO or VantageScore 4.0. Lenders could begin using VantageScore 4.0 as an alternative to Classic FICO for the first time.

Fannie Mae removed the minimum FICO score threshold from its Selling Guide for loans submitted through Desktop Underwriter, ending the decades-long 620 minimum for conventional loans at the GSE level.

In a joint announcement, HUD and FHFA confirmed that FICO 10T and VantageScore 4.0 are now available for FHA-insured mortgage underwriting in addition to conventional loans. This is described as the most significant change to mortgage credit scoring in decades.

Fannie Mae expects to publish historical FICO 10T scores in summer 2026. Broader lender adoption of both new models is expected through 2026, with Classic FICO continuing as an approved option during the transition.

2026 Is a Transition Year — Not Every Lender Has Switched

Not every lender is using the new models yet. During 2026, some lenders are using Classic FICO, some are using VantageScore 4.0, and some are evaluating FICO 10T. The lender you choose determines which model evaluates your application. This is why asking your lender which scoring model they use is now a critical question before you apply.

FICO 10T vs Classic FICO — Key Differences Side by Side

Here is a complete comparison of how FICO 10T differs from the Classic FICO models (FICO 5, FICO 2, FICO 4) currently used for most mortgages:

| Feature | Classic FICO | FICO 10T |

|---|---|---|

| Score range | 300–850 | 300–850 |

| Data horizon | Single snapshot — current month only | 24+ months of historical trend data |

| Credit utilization | Current utilization only | Current + trend direction over 24 months |

| Payment history | Yes — current report | Yes + behavioral consistency over time |

| Rent payment history | Not included | Included if reported to bureaus |

| Medical collections | Factored into score | Still factored in, reduced weight |

| Paid collections | Still hurt score (Classic FICO 5/2/4) | Less negative impact than older models |

| Personal loan use | Basic consideration | More nuanced — penalizes debt consolidation less |

| Mortgage use as of 2026 | Widely used — approved for Fannie/Freddie/FHA | Approved and being phased in — lender adoption in progress |

| Thin credit files | Harder to score with limited history | Trended data gives more insight on thin files |

| Created by | Fair Isaac Corporation | Fair Isaac Corporation |

What Is Trended Data and Why Does It Matter?

Trended data is the defining feature of FICO 10T — and it fundamentally changes how responsible credit behavior is rewarded. Understanding it fully is the most important thing you can do before applying for a mortgage in 2026.

Under Classic FICO, your credit utilization is a snapshot. If your credit card balance is $2,000 on a $10,000 limit on the day your score is pulled, your utilization for that card is 20%. The model records 20% and moves on. It does not know whether you had $8,000 on that card last year and have been paying it down, or whether you had $500 on it six months ago and have been spending aggressively.

FICO 10T knows the difference.

According to Experian, FICO 10T “can additionally consider whether your credit utilization rate has been increasing or decreasing over time.” This creates a dynamic score that reflects not just where you are financially, but where you are headed.

The Credit People describe the mechanical effect clearly: “When the average balance trends downward — because you consistently pay more than the minimum or keep usage under 30% — the model rewards you with a modest bump, often 5–10 points; the opposite occurs if balances climb month-to-month, which can shave a similar amount off your score.”

BNPL payments are also being incorporated into new FICO BNPL models — see our guide on how Klarna and BNPL affect your credit score in 2026 .

Real Example — How Trended Data Changes a Score

Under Classic FICO: A borrower with 30% utilization gets scored at 30% utilization. Period.

Under FICO 10T: The same borrower at 30% utilization gets scored differently depending on their trend. If utilization was 60% 18 months ago and has been steadily declining to 30% today, FICO 10T may reward that positive trend. If utilization was 10% 18 months ago and has been climbing to 30% today, FICO 10T may penalize that negative trend — even though both borrowers look identical on a Classic FICO snapshot.

This is why FICO describes 10T as providing lenders with “a more refined view of credit risk” — because two borrowers who look identical under Classic FICO can have meaningfully different risk profiles when their behavioral trends are considered.

Who Does FICO 10T Help — and Who Does It Hurt?

Not everyone benefits equally from FICO 10T. Your experience with the new model depends almost entirely on the direction of your credit behavior over the past 24 months. Here is an honest breakdown:

✅ FICO 10T Likely Helps You If…

- You have been consistently paying down credit card balances over the last 12–24 months

- Your credit utilization has been trending downward, even if your current rate is still moderate

- You pay rent and have enrolled in a rent reporting service — that history now counts

- You have a thin credit file with limited accounts but consistent positive payment behavior

- You recently paid off a personal loan used for debt consolidation

- You make payments above the minimum on revolving accounts consistently

- You have a long track record of on-time payments with no late marks in 24+ months

⚠️ FICO 10T May Hurt You If…

- Your credit card balances have been gradually increasing over the past 12–24 months, even without late payments

- You make only minimum payments consistently — FICO 10T identifies this as a risk signal

- Your utilization spikes regularly mid-month even if you pay in full each billing cycle

- You recently took out a personal loan to consolidate debt — FICO 10T watches this behavior closely

- You have had erratic payment patterns — some months great, some months minimal payments

- Your balances are the same as they were 24 months ago with no meaningful reduction

VantageScore Estimates 5 Million New Borrowers Benefit

According to the FHFA announcement, VantageScore estimates that approximately 5 million prospective buyers who could not be scored under Classic FICO will benefit from the new credit modeling — particularly first-time buyers with thin credit files, renters whose on-time payments were never counted, and immigrants with limited U.S. credit history.

Implementation Timeline — Where Are We Now in 2026?

Understanding where the mortgage industry currently sits in this transition matters because it affects the practical advice you should follow right now.

According to Alpine Banker’s analysis from May 2026, the practical takeaway is this: “2026 is a transition year. Some lenders are using the new models, some are sticking with Classic FICO, and many will support both. The framework is no longer ‘everyone uses the same score’ — it’s ‘lender choice within an approved set of models.'”

This means the lender you choose this year can determine which scoring model evaluates your application. That is not a theoretical difference — it can be the difference between approval and denial, or between a 6.5% rate and a 7.3% rate on a $350,000 home loan.

| Timeframe | What Is Happening | What It Means for You |

|---|---|---|

| Now (June 2026) | Lenders can choose Classic FICO or VantageScore 4.0. FICO 10T approved and being phased in by early adopters. | Ask your lender which model they use before applying. The answer may vary by lender. |

| Summer 2026 | Fannie Mae expects to publish historical FICO 10T scores for lender evaluation. | More lenders will begin side-by-side testing of FICO 10T vs Classic FICO. |

| Late 2026 | Broader lender adoption of new models expected. Classic FICO continues as approved option. | FICO 10T will become more widely used, but Classic FICO will remain valid. |

| 2027 and Beyond | Full transition to new scoring models with Classic FICO as fallback option. | Building positive credit trends now will benefit you as more lenders adopt FICO 10T. |

Rent and Utility Payments Under FICO 10T

One of the most significant improvements in FICO 10T over Classic FICO is its ability to incorporate rental payment history. For the approximately 44 million American households who rent their homes, this is potentially transformational.

Classic FICO completely ignores rent payments unless the landlord has set up a formal reporting relationship with a credit bureau — which the vast majority have not. A renter who has paid $2,000 per month on time for five years receives exactly zero credit for that behavior under Classic FICO. That same renter may have a thin credit file with a mediocre score despite being an extremely reliable payer.

FICO 10T incorporates rental payment history when it is reported to the credit bureaus. This benefits renters in two ways: it adds positive payment history to their record, and it provides 24 months of trended data showing consistent on-time payments — both of which feed directly into the FICO 10T algorithm.

Rent Must Be Actively Reported — It Does Not Happen Automatically

Most landlords do not automatically report rent payments to credit bureaus. To get your rent payments counted under FICO 10T, you need to either: (1) ask your landlord to enroll in a bureau reporting program, or (2) use a rent reporting service such as Rental Kharma, RentTrack, Boom Pay, or Experian RentBureau. Some services charge a monthly fee of $6–$10. Given that documented rent history could meaningfully improve your mortgage qualification, this investment is often worthwhile for renters planning to buy.

See What Mortgage You Qualify For at Your Score

Use our free Loan Affordability Calculator — enter your income, debts, and credit score to see estimated loan amount, rate range, and monthly payment for 2026 lender requirements.

FICO 10T vs VantageScore 4.0 — How They Differ

Both FICO 10T and VantageScore 4.0 are now approved for mortgage underwriting, and both use 24 months of trended data. But they are not identical. Understanding the differences matters if your lender gives you a choice or if you are comparing lenders who use different models.

| Feature | FICO 10T | VantageScore 4.0 |

|---|---|---|

| Created by | Fair Isaac Corporation | Equifax, Experian & TransUnion jointly |

| Score range | 300–850 | 300–850 |

| Trended data | Yes — 24 months | Yes — 24 months |

| Minimum credit history to score | 6 months of history, 1 account | 1 month of history, 1 account |

| Paid collections | Still factored in, reduced weight | Ignored entirely |

| Unpaid medical debt | Factored in | Ignored entirely |

| Rent payments | Included when reported | Included when reported |

| Lender familiarity | Very high — FICO is the industry standard | Growing — newer to mortgage underwriting |

| Who tends to benefit more | Borrowers with steady paydown history and no old collections | Borrowers with paid collections, thin files, or recent negative marks that are now resolved |

The key practical difference: if you have paid-off collections or unpaid medical debt on your report, VantageScore 4.0 will likely produce a higher score than FICO 10T, because it ignores paid collections entirely while FICO 10T still factors them in to some degree. If your report is clean but your behavior trends are strong, both models should produce similar results.

For a complete deep-dive into how VantageScore 4.0 works and who it benefits, see our VantageScore 4.0 guide .

Home Equity Products

The new models also apply to home equity products — see our HELOC credit score guide for how lender scoring model choices affect your HELOC application.

What to Do Before Applying for a Mortgage in 2026 — 7 Action Steps

The shift to multiple approved scoring models makes mortgage preparation more nuanced than it was in prior years. Here is exactly what to do in the months before you apply.

Ask Your Lender Which Scoring Model They Use

This is now a critical pre-application question. Ask: “Do you use Classic FICO, VantageScore 4.0, or FICO 10T for mortgage underwriting?” The answer determines everything about how your credit file will be evaluated. Some lenders may pull multiple scores. If your paid collections or thin file are a concern, seek lenders using VantageScore 4.0.

Focus on Trending Your Balances Downward — Starting Now

Under FICO 10T, the direction of your balances over the past 24 months is scored. If you are 12 to 18 months from applying for a mortgage, begin systematically paying down credit card balances now. Even if your current utilization is already reasonable at 30%, reducing it to 20% and then 10% over the coming months creates a positive trend that FICO 10T will reward.

Never Make Only the Minimum Payment on Revolving Accounts

FICO 10T identifies minimum payment behavior as a risk signal. Consistently paying only the minimum — even without any late payments — can reduce your FICO 10T score compared to making larger payments. Always pay at least double the minimum, or ideally the full balance, each month.

Enroll in Rent Reporting if You Are a Renter

If you have been renting and paying on time, this history is invisible to Classic FICO but visible to FICO 10T and VantageScore 4.0 if reported. Sign up for a rent reporting service — Rental Kharma, RentTrack, or Boom Pay — at least 12 months before applying for a mortgage to build a reported rent history. Some services can retroactively report up to 24 months of history.

Pull Your Full Credit Report and Check for Errors

Get your free credit reports from all three bureaus at AnnualCreditReport.com. Look specifically for: collection accounts that should have been removed under 2026 medical debt rules, any items past their 7-year removal date, and accounts you do not recognize. Errors affect all scoring models. Dispute anything inaccurate before applying.

Pay Off Old Collections Before Applying

Under Classic FICO, paying old collections had mixed impact because the account still appeared on your report. Under FICO 10T, paid collections carry less negative weight. Under VantageScore 4.0, paid collections are ignored entirely. If a lender is using newer models, paying off a collection before applying may meaningfully improve your qualifying score.

Do Not Open New Credit in the 6 Months Before Applying

This advice applies to both Classic FICO and FICO 10T. New credit applications trigger hard inquiries, lower your average account age, and signal financial instability. In the 6 months before a mortgage application, avoid opening new credit cards, taking out personal loans, or co-signing any debt. Let your existing positive trends build without disruption.

See How a Specific Action Would Change Your Score

Use our free Credit Score Impact Simulator to see the estimated point impact of paying off a balance, removing a collection, or opening new credit — before you make the move.

See Mortgage credit score guide for 2026

For minimum score requirements by loan type, see our complete mortgage credit score guide for 2026.

Frequently Asked Questions

What is FICO 10T?

FICO 10T is the tenth generation of the FICO scoring model. The “T” stands for trended data — meaning it analyzes 24 months of your credit behavior rather than a single snapshot. It was validated by FHFA in 2022 for mortgage use and became available to lenders in 2026 alongside VantageScore 4.0. Like Classic FICO, it produces a score from 300 to 850.

Is FICO 10T required for mortgages in 2026?

Not required — but now permitted. As of April 2026, lenders selling loans to Fannie Mae, Freddie Mac, and FHA can choose between Classic FICO or VantageScore 4.0, with FICO 10T approved and being phased in. Classic FICO remains a valid option. During 2026, the model your lender uses depends on which one they have implemented — making it important to ask before applying.

Will FICO 10T raise or lower my credit score?

It depends entirely on your behavior trends over the past 24 months. If your balances have been consistently decreasing, FICO 10T will likely produce a higher score than Classic FICO for you. If your balances have been increasing or you have been making only minimum payments, FICO 10T may produce a lower score. The key factor is the direction of your credit behavior, not just your current snapshot.

What is the minimum credit score for a mortgage in 2026?

Fannie Mae removed the minimum FICO score threshold from its Selling Guide in November 2025. However, individual lenders still set their own minimum thresholds. In practice, most lenders require 620 to 640 for conventional loans and 580 (with 3.5% down) for FHA loans. The best mortgage rates in 2026 still require 740 or above, regardless of which scoring model is used.

How do I know which scoring model my lender will use?

Ask directly before applying. The exact question to ask is: “Which credit scoring model do you use for mortgage underwriting — Classic FICO, VantageScore 4.0, or FICO 10T?” During 2026, lenders will use different models depending on what they have implemented. The lender you choose can affect which scores are evaluated, making this one of the most important questions to ask when shopping for a mortgage.

Does FICO 10T include rent payments?

Yes — but only if your rent is being reported to the credit bureaus. Most landlords do not automatically report rent. To get credit for your rent payment history under FICO 10T, enroll in a rent reporting service such as Rental Kharma, RentTrack, Boom Pay, or Experian RentBureau. Some services can retroactively add up to 24 months of rent history, which can meaningfully improve your score under trended models.

How is FICO 10T different from VantageScore 4.0?

Both use 24 months of trended data and are approved for mortgage underwriting. Key differences: VantageScore 4.0 completely ignores paid collections, while FICO 10T still factors them in to a reduced degree. VantageScore can score consumers with as little as one month of history, while FICO 10T requires six months. Borrowers with paid collections or thin files tend to benefit more from VantageScore 4.0; borrowers with clean files and strong paydown trends tend to do well under both.

Related Free Tools

Related Guides

- Federal Housing Finance Agency — Credit Scores Policy Page

- Fannie Mae — Credit Score Models and Reports Initiative

- myFICO.com — FICO Score Versions

- Experian — FICO Score 10 Changes Explained

- FHFA and HUD Joint Announcement — April 22, 2026

- Alpine Banker — VantageScore 4.0 & FICO 10T: 2026 Mortgage Changes

- MBA NewsLink — FICO Score 10T Adopter Program, March 2026

1 thought on “FICO 10T vs Classic FICO: What Changes for Your Mortgage in 2026 — Complete Guide”