Why Your Credit Score Dropped in 2026 — And How to Fix It Fast

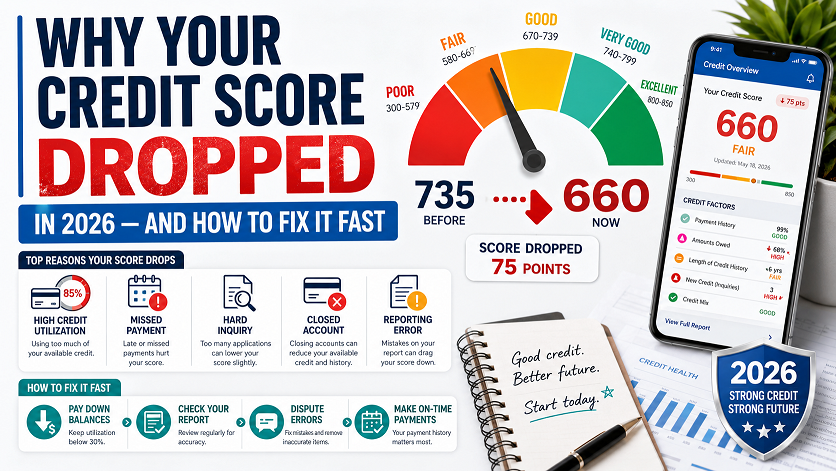

The average FICO score in America fell to 715 in 2025 — the second consecutive year of declines — and scores are under continued pressure in 2026. The top causes are: student loan delinquencies, high credit card utilization, new collection accounts, missed payments, hard inquiries, BNPL reporting, and rising mortgage delinquencies. Some of these can be fixed in 30 days. Others take longer. This guide covers all 9 causes and gives you the fastest proven fix for each one.

If your credit score dropped recently, you are not alone — and it is not necessarily your fault. American credit scores have been declining for two straight years. The causes are partly economic, partly systemic, and partly the result of new reporting rules that most people were never warned about.

But a dropped score is not permanent. Some of the most damaging causes have surprisingly fast fixes. The key is knowing exactly which cause applies to your situation — and then taking the right action, not just any action.

This guide walks you through every major reason credit scores are dropping in 2026, tells you how fast each one can be reversed, and gives you a concrete action plan for each scenario.

Why Credit Scores Are Falling Nationally in 2026

Understanding the big picture helps you put your own situation in context. The decline in average FICO scores since 2023 is driven by several overlapping forces — not a single cause.

The net result: more Americans have negative items appearing on their reports in 2026 than at any point since the early post-pandemic period. If your score dropped, you are experiencing a trend that millions of households share — but the fix is still specific to your situation.

The 9 Most Common Reasons Your Score Dropped in 2026

Every credit score drop has a specific cause — or a combination of causes. Here are the nine most common in 2026, ordered by how severely each one typically damages your score, with the fastest fix for each.

Payment history is the single largest factor in your credit score — 35% under Classic FICO. A single payment reported 30 days late can drop a good credit score by 60 to 110 points. The longer the delinquency (60 days, 90 days, 120+ days), the more damage it does. In 2026, student loan payments are a leading cause — many borrowers believed they were in some form of protection or deferment that had actually ended.

Pay the overdue amount immediately to stop the delinquency from aging further. Then call the lender and request a goodwill adjustment — ask them to remove the late payment notation in exchange for your otherwise strong payment record. This works more often than most people expect, especially for first-time lates with long-standing lenders. Your score will not recover overnight, but stopping the damage now limits its long-term impact. See our goodwill letter templates for exact wording.

When an unpaid debt is sold or transferred to a collections agency, that agency typically reports a new collection account to the bureaus. This is one of the most damaging events for a credit score. Common sources in 2026: medical bills of $500 or more (the CFPB rule that would have removed these was vacated), old utility accounts, gym memberships, and telecom bills. The collection often appears with no warning — many people discover it when their score drops suddenly.

First, verify the debt is legitimate and the amount is accurate — billing errors are extremely common, especially in medical collections. Do not pay a collection without first requesting debt validation in writing via certified mail. If it is accurate and you want it removed, negotiate a pay-for-delete agreement in writing before paying — some collection agencies will remove the tradeline in exchange for full or partial payment. If the debt is paid already or under $500 (for medical), dispute it with the bureau immediately as it should have been removed. See our pay-for-delete letter guide.

Credit utilization — how much of your available revolving credit you are using — accounts for 30% of your Classic FICO score. When utilization crosses 30%, scores begin to fall. When it crosses 50% or 70%, the drop accelerates. This is particularly common in 2026 as household budgets have been squeezed by inflation and higher interest rates, pushing more spending onto credit cards. Even if you pay your cards on time every month, a high balance relative to your limit can still hurt your score significantly.

This is the fastest-recovering cause of a score drop. Pay down your balances to below 30% of your credit limit — ideally below 10% for maximum score recovery. Your score will improve as soon as the new lower balance is reported to the bureaus, typically within 30 days. If you cannot pay down the balance immediately, call your card issuer and request a credit limit increase — increasing your limit without increasing your balance automatically lowers your utilization ratio. Do not close any existing cards, as this reduces available credit and worsens utilization. Use our utilization calculator to find your exact target paydown amount.

Student loans returning to active repayment after forbearance — and the subsequent delinquency reporting for borrowers who missed payments — is one of the biggest drivers of score drops nationally in 2025 and 2026. Many borrowers were unaware that protection periods had ended, or believed they were enrolled in income-driven repayment plans that had not been properly processed. A 90-day student loan delinquency is one of the most damaging single events a credit file can experience.

Contact your loan servicer immediately — do not wait. Ask specifically about: (1) income-driven repayment plans that would set your payment to $0 if your income qualifies, (2) deferment or forbearance options to stop the delinquency from aging further, and (3) student loan rehabilitation, which can remove the delinquency notation from your credit report after nine months of on-time payments on a rehabilitated loan. The single most important thing is to stop the late payment from aging to 90 days or beyond — each aging milestone does additional damage. See our dedicated guide: Student Loans and Your Credit Score in 2026.

Every time you apply for credit — a credit card, auto loan, mortgage, personal loan — the lender pulls a hard inquiry on your credit report. Each hard inquiry typically drops your score 5 to 10 points. Multiple inquiries in a short period outside rate-shopping windows can add up to a meaningful drop. In 2026, this is particularly relevant for borrowers who have been shopping aggressively for mortgage rates or auto financing as market conditions shift.

Hard inquiries cannot be removed unless they were made without your authorization — in which case, dispute them with the bureau immediately as unauthorized. For legitimate inquiries, the only fix is time: inquiries stop affecting your score after 12 months and fall off your report entirely after 24 months. To limit future damage, do all your rate shopping within a 14–45 day window — multiple mortgage or auto inquiries in this window are treated as a single inquiry by most scoring models. Avoid applying for new credit cards or personal loans in the 3–6 months before a major credit application.

Closing a credit card — whether you closed it yourself or the issuer closed it for inactivity — can hurt your score in two ways. First, it reduces your total available credit, which raises your utilization ratio. Second, if it was one of your older accounts, it can reduce the average age of your credit history over time. Issuers are increasingly closing inactive cards in 2026, catching some cardholders off guard with an unexpected score drop.

If the issuer closed the card, call and ask for reinstatement — some will reopen recently closed accounts, especially if you have a good history with them. To prevent future closures, make at least one small purchase per year on any card you want to keep open. If you are planning to close a card yourself, avoid closing your oldest card and avoid closing any card that carries a large portion of your available credit. The utilization impact of a closed card recovers as you pay down other balances.

Buy Now Pay Later is one of the newest and most underappreciated causes of credit score drops in 2026. Several major BNPL providers — including Klarna and others — now report payment activity to credit bureaus. Many consumers treat BNPL purchases casually, not realizing that a missed installment can generate a negative mark on their credit report just like a missed credit card payment. Under VantageScore 4.0, BNPL accounts are now factored into scoring models used for mortgage underwriting.

Pay any overdue BNPL installments immediately — the faster you clear the delinquency, the less damage it does as it ages. Set up autopay on all active BNPL plans going forward. Check your credit report to see exactly which BNPL accounts are reporting and in what status. If a BNPL account is showing incorrectly — for example, showing as unpaid when you did pay — dispute it with the reporting bureau directly. Treat every active BNPL plan as a credit account from this point forward. See our full guide: Does Klarna Affect Your Credit Score in 2026?

Smaller medical debts (under $500) and paid medical collections were removed from credit reports under the bureaus’ 2023 voluntary policy — and those changes are still in effect. However, the CFPB’s broader rule that would have removed all medical debt was vacated by a federal court in July 2025. This means unpaid medical collections of $500 or more can still appear on your report and damage your score. In 2026, this is still catching many consumers off guard who believed all medical debt had been removed.

First, verify the debt — medical bills are among the most error-prone items on credit reports. Request debt validation from the collection agency before paying anything. If you live in one of the 15 states with their own medical debt reporting bans, dispute the collection with the bureau citing your state’s law. If the debt is accurate, negotiate a pay-for-delete agreement in writing before paying. If you cannot afford to pay, check whether the original hospital or provider has a financial assistance program — many do, and qualifying can eliminate the debt entirely. Full details: Medical Debt Credit Report Guide 2026.

Studies consistently find that a significant percentage of credit reports contain at least one error — and errors that hurt scores are more common than most people realize. In 2026, common errors include: accounts from identity theft that do not belong to you, duplicate negative entries for the same debt, incorrect payment statuses, accounts showing as open that were closed, and outdated negative items past their 7-year reporting window. If your score dropped and you cannot identify a clear cause in your own financial behavior, an error or fraud account may be the culprit.

Pull your full credit reports from all three bureaus at AnnualCreditReport.com and review every account. For errors, file a dispute online with the bureau directly — Equifax, Experian, and TransUnion are all required to investigate within 30 days. For identity theft, place a fraud alert or credit freeze immediately at all three bureaus (freezes are free), then file a report at IdentityTheft.gov. Disputed errors that are confirmed as inaccurate must be removed — and the score recovery from removing a major error can be immediate and significant. See our step-by-step dispute guide.

How Fast Can You Recover — By Cause

Recovery time is the question everyone asks first. Here is an honest breakdown. The good news: some of the most common causes recover surprisingly fast. The bad news: the most damaging causes are the slowest to heal.

Pay down balances below 30%. Score recovers in the next reporting cycle — the fastest win available.

File a dispute. Bureaus must investigate within 30 days. If removed, score recovers immediately.

Impact fades after 12 months. Inquiries fall off the report entirely after 24 months.

Depends on how much available credit was lost. Pay down other balances to offset utilization impact.

Pay immediately to stop aging. Impact diminishes with consistent on-time payments going forward.

Impact fades significantly after 2 years of clean payments. Falls off report after 7 years.

Impact diminishes over time. Falls off report 7 years from original delinquency date. Pay-for-delete can accelerate removal.

Chapter 13: 7 years. Chapter 7: 10 years. Score can meaningfully recover in 2–3 years with the right rebuilding steps.

Step 1: Find Out Exactly Why Your Score Dropped

Before taking any action, you need to know exactly what caused the drop. Guessing wastes time and sometimes makes things worse — for example, paying a collection without a pay-for-delete agreement may actually prevent you from ever getting it removed.

Pull All 3 Credit Reports — Free

Go to AnnualCreditReport.com and pull your full report from Equifax, Experian, and TransUnion separately. You can now pull all three for free weekly. Each bureau may show different information — a collection may be on one report but not the others. Review every section: payment history, balances, collections, inquiries, and account status.

Check the “Score Factors” on Your Score Report

Every credit score comes with reason codes — also called score factors — that explain the top items dragging your score down. When you check your score through Experian, Credit Karma, or your bank’s free credit score tool, look for the list of negative factors. These are ranked in order of impact and tell you exactly what the scoring model is penalizing you for right now. This is your prioritized action list.

Compare Your FICO Score vs VantageScore

Check both your FICO Score 8 (available free via Experian) and your VantageScore (available free via Credit Karma). A large gap between them — with VantageScore notably higher — often signals medical collections or BNPL accounts that VantageScore ignores but Classic FICO penalizes. This gap is important context if you are planning to apply for a mortgage — your lender’s choice of scoring model matters enormously.

Check Dates Against the 7-Year Reporting Window

For every negative item you find, note the date of first delinquency — the date the original account first went past due. Negative items must be removed from your credit report 7 years after that date under the Fair Credit Reporting Act. If any negative item on your report is past its 7-year window, dispute it immediately for automatic removal — this is one of the easiest wins in credit repair.

The Fastest Fixes — What You Can Do This Week

Not every fix takes months. Here are the actions that can produce measurable score improvement within 30 to 60 days:

| Action | Time to Impact | Difficulty | Potential Gain |

|---|---|---|---|

| Pay down credit card balances below 30% utilization | 30 days | Moderate (requires funds) | 20–50 pts |

| Dispute inaccurate negative items with bureaus | 30–45 days | Easy (online process) | Up to 100+ pts if item is removed |

| Add Experian Boost (rent, utilities, streaming) | Immediate | Very easy (free) | 10–20 pts (Experian FICO only) |

| Request credit limit increase (without hard pull) | 7–14 days | Easy (call your issuer) | 10–30 pts (improves utilization) |

| Become an authorized user on a strong account | 30–60 days | Easy (ask a trusted person) | 20–50 pts |

| Negotiate goodwill removal of a late payment | 30–60 days | Moderate (requires letter/call) | 40–80 pts if successful |

| Negotiate pay-for-delete on a collection | 30–60 days | Moderate (requires negotiation) | 50–100 pts if successful |

| Dispute outdated items past 7-year window | 30–45 days | Easy (online dispute) | Varies — item must be removed |

Does the Scoring Model Matter for Your Drop?

In 2026, the answer is yes — more than ever. The scoring model a lender uses can determine whether certain negative items on your file hurt your qualification at all.

The Model Your Lender Uses Can Change Everything

Under Classic FICO (5, 2, 4) — still used by many mortgage lenders — medical collections, BNPL accounts, and paid collections can all factor into your score. Under VantageScore 4.0 — now approved for Fannie Mae, Freddie Mac, and FHA mortgages — medical collections are ignored entirely and BNPL history is factored in differently. The same borrower with the same credit file can have a meaningfully different score depending on which model is applied. Before applying for a mortgage in 2026, ask your lender which model they use — the answer affects your strategy.

| Negative Item | Classic FICO Impact | VantageScore 4.0 Impact |

|---|---|---|

| Medical collections (any amount) | Significant negative impact | Ignored entirely |

| Paid collections | Reduced impact vs unpaid | Lower weight |

| BNPL payment history | Varies by how account is classified | Factored in — missed payments matter |

| Rent payment history | Not factored in (Classic FICO) | Can help with VantageScore 4.0 |

| Trended utilization data | Snapshot only (Classic FICO 8) | 24-month trend factored in (FICO 10T, VS 4.0) |

Student Loans and Credit Scores in 2026 — What You Need to Know

Student loan debt is one of the biggest contributors to the national score decline — and one of the most misunderstood. Here is what is actually happening and what you can do about it.

The Forbearance-to-Delinquency Pipeline Is Still Hurting Scores in 2026

Millions of borrowers experienced a gap between the end of federal student loan payment pauses and the start of income-driven repayment plans being properly processed. Many made no payments during this gap — and some of those missed payments were eventually reported to credit bureaus as delinquencies. If you believe your student loan delinquency resulted from a servicer error, processing delay, or misapplied forbearance, you may have grounds for a dispute or a borrower defense claim. Contact your servicer and request a complete payment history before assuming the delinquency is accurate.

If you have student loan delinquencies on your report, here are your main options in order of how quickly they can help your score:

- Enroll in income-driven repayment (IDR) — this sets your monthly payment based on income, potentially to $0, and stops new delinquencies from accruing immediately

- Rehabilitate defaulted loans — after nine months of on-time payments under a rehabilitation agreement, the default notation is removed from your credit report (though the late payments before default remain)

- Consolidate defaulted loans — Direct Consolidation can bring a defaulted loan into good standing faster than rehabilitation, but does not remove the negative history

- Dispute servicer errors — if you were in a deferment or forbearance that was not properly applied, the resulting delinquency may be removable as an error

BNPL and Credit Scores in 2026 — The Risk Most People Miss

Buy Now Pay Later services have become mainstream — and in 2026, their credit reporting implications have become real. This is one of the newest and most underappreciated causes of credit score drops.

Treat Every BNPL Plan as a Credit Account — Because It Now Is One

Several major BNPL providers now report to credit bureaus. Under VantageScore 4.0 — now approved for mortgage underwriting — BNPL accounts are factored into your score. Under older FICO models, reporting varies by provider and how the account is classified. In either case: a missed BNPL installment that reaches 30 days past due and is reported to the bureaus can drop your score by 20 to 60 points, exactly like a missed credit card payment. The casual, low-stakes feeling of splitting a $200 purchase into four payments does not change the credit reporting reality.

The safest approach to BNPL in 2026:

- Set up autopay for every active BNPL plan — treat each installment like a bill payment, not an optional choice

- Keep track of all active BNPL plans in a single place — it is easy to forget a plan that started months ago

- Check your credit report regularly for BNPL accounts and their reported status

- Limit the number of active BNPL plans — having many open simultaneously increases the risk of a missed payment

- If you miss a payment, pay immediately — every day of additional delinquency increases damage

See How Removing a Negative Item Affects Your Score

Use our free Score Impact Simulator — enter your negative items and see the estimated score impact of paying down balances, removing collections, or disputing errors.

Frequently Asked Questions

Why did my credit score drop suddenly in 2026?

The most common reasons for a sudden drop include: a new hard inquiry from a credit application, a missed or late payment just reported, a spike in your credit utilization ratio, a new collection account appearing, an old account being closed, or a student loan returning to delinquent status. Pull your credit reports at AnnualCreditReport.com to identify the specific cause before taking action.

How much can a credit score drop in 2026?

It depends on the cause and your starting score. A single missed payment can drop a good score 60–110 points. A new collection account can drop it 50–100 points. A bankruptcy can drop it 130–240 points. Hard inquiries typically drop scores 5–10 points each. High credit utilization above 30% can drop scores 20–50 points. The higher your starting score, the more you stand to lose from a single negative event.

How long does it take to recover a dropped credit score?

Recovery time depends on the cause. High utilization can recover in 30 days once you pay down balances. A hard inquiry fades in 12 months. A missed payment takes 7 years to fall off but its impact fades significantly after 2 years of on-time payments. A collection account takes 7 years to fall off. For most drops caused by utilization or inquiries, significant recovery is possible within 3–6 months with consistent action.

Did average credit scores drop in 2026?

Yes. The average FICO score fell to 715 in 2025, the second consecutive year of decline from the pandemic-era peak of 718 in 2023. Scores are under continued pressure in 2026 due to rising mortgage delinquencies, student loan repayment challenges, increased credit card utilization, and economic pressure on subprime borrowers. If your score dropped, you are part of a national trend — not alone in your situation.

Can I fix a credit score drop fast in 2026?

Some fixes are genuinely fast. Paying down credit card balances below 30% utilization can recover points in 30 days. Disputing and removing an inaccurate negative item can add points within 30–45 days. Adding Experian Boost can add points immediately. Getting added as an authorized user on a strong account can add points within one billing cycle. Fixes for genuine delinquencies, collections, and bankruptcies require consistent positive behavior over 12–24 months.

Do student loans hurt your credit score in 2026?

Only if they are delinquent. Student loans paid on time contribute positively to your payment history and credit mix. The problem in 2025 and 2026 is that many borrowers missed payments after forbearance periods ended, and those missed payments were reported to the bureaus. A single 90-day student loan delinquency can drop a score 60–100 points. Contact your loan servicer immediately about income-driven repayment or loan rehabilitation if your student loans are delinquent.

Does BNPL hurt your credit score in 2026?

It can — if you miss payments. Several major BNPL providers now report to credit bureaus, and under VantageScore 4.0 (now approved for mortgage underwriting), BNPL accounts are factored into scoring. A missed BNPL installment that is reported can drop your score 20–60 points. Treat every BNPL plan like a credit account: set up autopay, pay on time, and monitor your credit report for BNPL tradelines.

Related Free Tools

Related Guides

- Equifax — April 2026 Consumer Pulse: The Latest Consumer Credit Trends

- Stacker — What’s in Store for Our Money in 2026

- FICO — Credit Score Education: What Goes Into a Credit Score

- Experian — Average Credit Score in America

- CFPB — Consumer Financial Protection Bureau Official Blog

- VantageScore — VantageScore 4.0 Fact Sheet

- Berkeley Consumer Law Center — Court Overturns Federal Rule That Keeps Medical Debt Off Credit Reports

1 thought on “Why Your Credit Score Dropped in 2026 (And How to Fix It Fast)”