HELOC Credit Score Requirements 2026 — What Score You Need, Current Rates, and How to Qualify

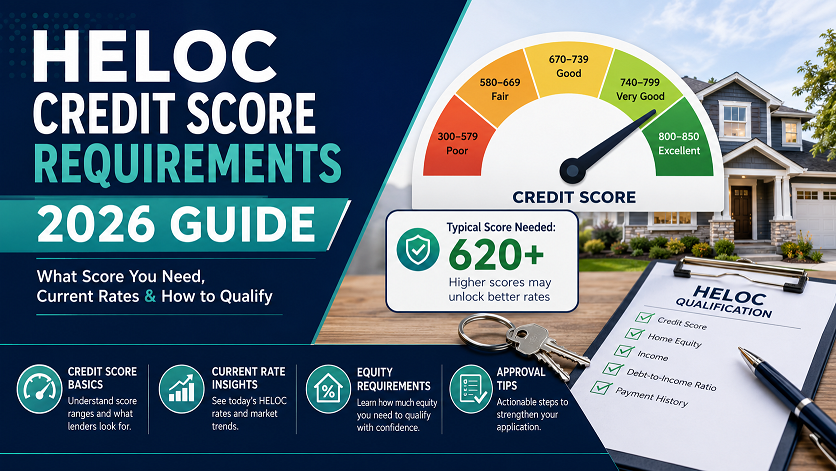

The minimum credit score for a HELOC in 2026 is 620 at most lenders — but only 4.6% of HELOCs go to borrowers below that threshold, meaning lenders strongly favor 660 to 680 for standard approval. To get the best HELOC rates, you need 700 or higher — ideally 740+. The national average HELOC rate is 7.21% as of June 2026 (Curinos). Beyond credit score, you also need at least 15–20% equity in your home, a DTI below 43%, and verifiable income. This guide covers every requirement in full.

2026 is one of the best years in recent memory to tap home equity. The national average HELOC rate has fallen from over 10% in early 2024 to 7.21% in June 2026 — and millions of American homeowners are sitting on record levels of home equity built up during the pandemic-era housing surge.

But HELOC credit requirements are stricter than most people expect. Unlike a first mortgage — where FHA and VA programs offer significant flexibility for lower-credit borrowers — a HELOC is a second lien on your home. That means lenders are more selective. A 620 score might get you in the door, but you will pay a rate premium that can cost thousands over the draw period.

This guide tells you exactly where you stand at your current credit score, what rate you can realistically expect in 2026, and what to do if your score is not quite where lenders want it.

Credit Score Requirements — 4 Tiers and What Each Gets You

The minimum credit score for a home equity line of credit in 2026 is 620 at most traditional banks and credit unions, but that floor only gets you in the door. Borrowers at 660–680 qualify for standard approval, while 700–720+ unlocks meaningfully lower rates.

Most lenders decline. Only 4.6% of HELOCs issued go to borrowers below this line. Focus on rebuilding before applying.

Limited lender options. You need strong equity (25%+), low DTI, and clean payment history to compensate. Rates are 1–2% above prime borrowers.

Most HELOC lenders approve here. Rates are competitive but not optimal. 15–20% equity required. Good approval odds at credit unions.

All lender options available. Best rates at 740+. Wide lender choice, highest credit lines, most flexible terms. This is where you want to be.

Why HELOC Requirements Are Stricter Than First Mortgage Requirements

A HELOC is a second-lien loan. This means if you default and the home is foreclosed, the HELOC lender is second in line to recover their money — after your primary mortgage lender. That increased risk is why HELOC lenders require higher credit scores than many first mortgage programs. A borrower who qualifies for an FHA loan at 580 may not qualify for a HELOC until they reach 620 to 640.

Current HELOC Rates by Credit Score — June 2026

The national average HELOC adjustable rate is 7.21% as of June 2026 according to Curinos, while Bankrate’s survey of major lenders puts the national average at 7.43% as of June 3, 2026. But these averages are based on strong-credit borrowers with low LTV ratios. Here is what different credit tiers actually see:

*Monthly payments shown as interest-only during draw period on $100,000 balance. Rates are illustrative estimates based on typical credit tier premiums. Actual rates vary by lender, LTV, and individual profile. Base rate source: Curinos/Bankrate, June 2026.

The Real Cost of a Lower Score on a HELOC

The difference between a 760 and 640 credit score costs $2,000 per year, or $20,000 over 10 years on a $100,000 balance. On a $150,000 HELOC, that gap grows to $30,000 over the draw period. Spending 3 to 6 months improving your score before applying is not just worth it — it is one of the highest-return financial moves you can make as a homeowner.

Home Equity Requirements — How Much You Need for a HELOC

Your credit score gets you in the door, but your home equity determines how much you can borrow and at what terms. Most lenders require at least 15–20% equity in your home, with most lenders capping combined loan-to-value at 85%.

Example: $400,000 home value | $200,000 mortgage (50% LTV) | Max HELOC at 85% CLTV = $140,000 | Required equity retained = $60,000 (15%)

HELOC Borrowing Formula

Here is the simple calculation lenders use:

Maximum HELOC = (Home Value × Maximum CLTV%) − Existing Mortgage Balance

| Home Value | Mortgage Balance | Max CLTV | Maximum HELOC | Equity Remaining |

|---|---|---|---|---|

| $300,000 | $180,000 | 85% | $75,000 | $45,000 (15%) |

| $400,000 | $200,000 | 85% | $140,000 | $60,000 (15%) |

| $500,000 | $250,000 | 85% | $175,000 | $75,000 (15%) |

| $400,000 | $340,000 | 85% | $0 — insufficient equity | Only 15% equity total |

| $500,000 | $200,000 | 80% (lower-credit) | $200,000 | $100,000 (20%) |

Lower Credit Score = Lower Maximum CLTV

If your credit score is on the lower end — 620 to 660 — lenders typically reduce the maximum CLTV they allow, from 85% down to 75% or 80%. This means you need more equity to access the same loan amount. A borrower with a 740 score might access 85% CLTV, while a 630-score borrower at the same lender might be capped at 75% CLTV — requiring significantly more equity to borrow the same amount.

Full HELOC Requirements Checklist 2026

Credit score and equity are the two biggest factors, but lenders evaluate several other criteria before approving a HELOC:

| Requirement | Standard 2026 Threshold | Notes |

|---|---|---|

| Credit score | 620 minimum | 680+ preferred | 740+ for best rates | Varies significantly by lender — large banks often require 680–700 |

| Home equity | 15–20% minimum (CLTV max 80–85%) | Lower-credit borrowers may need 25%+ equity as compensating factor |

| Debt-to-income ratio | 43% maximum | Some lenders allow up to 50% with strong equity and credit |

| Income verification | 2 years of stable, verifiable income | W-2s, pay stubs, or 2 years of tax returns for self-employed |

| Payment history | No late payments in last 12–24 months | Especially mortgage payment history — any missed mortgage payments are disqualifying for most lenders |

| Property type | Primary residence, second home, some investment properties | Rates are highest for investment properties — some lenders only do primary residences |

| Home appraisal | Required by most lenders | Some lenders use automated valuation models (AVM) to skip full appraisal — faster and cheaper |

| Title insurance | Required | Part of closing costs — typically $200–$500 |

| Minimum draw | Varies — often $10,000–$25,000 | Some lenders require a minimum initial draw at closing |

Lender-by-Lender Credit Score Requirements for HELOCs in 2026

HELOC credit requirements vary significantly by lender type. Large national banks like Chase, Bank of America, Wells Fargo, and U.S. Bank typically require higher credit scores — minimum 680–700 for approval and 720+ for best rates — because they focus on lower-risk borrowers and can afford to be selective. Online lenders use automated underwriting and have lower overhead, making them more flexible — typically 620–660 minimum for approval.

| Lender Type | Typical Min. Score | Max CLTV | Best For |

|---|---|---|---|

| Large national banks Chase, BofA, Wells Fargo, US Bank |

680–700 | 80–85% | Borrowers with 700+ scores who want full-service banking relationship |

| Regional banks PNC, Regions, KeyBank, Truist |

660–680 | 80–85% | Mid-range credit borrowers in bank’s service area |

| Credit unions Navy Federal, PenFed, local CUs |

620–640 | 85–90% | Members with 620–680 scores — most flexible terms for qualifying members |

| Online lenders Figure, Spring EQ, Achieve |

620–640 | 85–95% | Speed (some close in 5 days), borrowers with 620–680, higher LTV needs |

| Mortgage companies Freedom Mortgage, LoanDepot |

640–660 | 80–85% | Existing mortgage customers, convenience-focused borrowers |

Credit Unions Are Your Best Option at 620–660

If your credit score is between 620 and 660, credit unions are the most HELOC-friendly lenders. Many credit unions allow CLTV up to 90%, require lower minimum scores than banks, and offer member-favorable rates. Navy Federal Credit Union, PenFed, and local credit unions are worth applying to first if your score is near the lower threshold. If you are not already a member, most credit unions allow you to join with a small donation to an affiliated nonprofit.

HELOC vs Home Equity Loan — Which Is Right for You?

Both products let you access your home equity, but they work very differently. The right choice depends on how you plan to use the funds:

HELOC — Best For Ongoing Needs

- Variable rate — adjusts with Prime Rate

- Revolving credit line — draw, repay, draw again

- 10-year draw period, then 20-year repayment

- Interest-only payments during draw period

- Current national average: 7.21% (Curinos)

- Best for: Home renovations over time, ongoing expenses, emergency fund, business costs

- Risk: Rate can rise — plan for payment increases

Home Equity Loan — Best For One-Time Needs

- Fixed rate — locked for entire term

- Lump sum disbursement — all funds at closing

- Fixed monthly payments — predictable budget

- 5 to 30-year repayment term

- Current national average: 7.36% (Curinos)

- Best for: Single large expense — debt consolidation, major renovation, tuition

- Risk: Higher initial payment since you pay principal from day one

HELOC vs Cash-Out Refinance — The Key 2026 Decision

With primary mortgage rates hovering above 6% in 2026, this decision is more important than in prior years. For homeowners with low primary mortgage rates and a chunk of equity in their house, it is probably one of the best times to get a HELOC or a home equity loan. You do not give up that great mortgage rate, and you can use the cash drawn from your equity for things like home improvements, repairs, and upgrades.

| Factor | HELOC | Cash-Out Refinance |

|---|---|---|

| Replaces existing mortgage? | No — keeps your current rate | Yes — entire mortgage at current rates |

| Rate type | Variable (Prime + margin) | Fixed (typically lower than HELOC) |

| Closing costs | Low — $0 to $500 at many lenders | High — 2% to 5% of loan amount |

| Min. credit score | 620–680 | 580 (FHA cash-out) or 620 (conventional) |

| Flexibility | Draw only what you need, when you need it | Lump sum only |

| Best if current mortgage rate is… | Below 5.5% — keep your rate, add HELOC | Above 6.5% — refinance lowers overall cost |

The Golden Rule for 2026 Home Equity Decisions

If your existing mortgage rate is below 5%, a HELOC almost always beats a cash-out refinance in 2026. Replacing a 3.5% mortgage with a 6.7% mortgage to access equity means paying a much higher rate on your entire mortgage balance — not just the equity you pull out. The HELOC lets you keep your low first mortgage while accessing the equity at current second-lien rates. Run the numbers with your specific loan amount before deciding.

See What HELOC Amount You Could Qualify For

Use our free Loan Affordability Calculator — enter your income, existing debts, and credit score to see your estimated qualification range and monthly payment at current 2026 HELOC rates.

How to Get a HELOC with Lower Credit — 5 Strategies

If your score is in the 620–659 range, you are not automatically disqualified — but you need to compensate with strength in other areas. At 620, you need to make up for the lower score by being strong in other areas: a strong income, a low debt-to-income ratio below 36%, a lot of home equity above 20%, and a clean payment history for the last 12 to 24 months.

Apply With Credit Unions and Online Lenders First

Large banks typically set their HELOC minimum at 680 to 700 — 60 to 80 points above the program floor. Credit unions and online lenders operate closer to the 620 minimum. Apply with at least 3 to 5 lenders across different types before concluding you cannot qualify. The variation between lenders at a 640 score can be the difference between approval at 8.5% and outright rejection.

Maximize Your Equity Position

The more equity you have, the less risk the lender takes. A borrower with a 640 score and 35% equity is a much safer bet than a 640-score borrower at 20% equity. If you are near a major home equity milestone — say, 25% vs 20% — consider waiting until after your next mortgage payments bring you there before applying. Some lenders will approve at 640 with 25%+ equity who would decline at 20%.

Reduce Your DTI Before Applying

HELOC underwriters look hard at your DTI — including your estimated HELOC payment added to your existing monthly obligations. Paying off a car loan or credit card balance before applying can meaningfully reduce your DTI and improve your approval odds. A DTI below 36% is the sweet spot that compensates for a lower credit score in most HELOC underwriting scenarios.

Consider a Smaller Credit Line

Requesting a smaller HELOC — $50,000 vs $100,000 — reduces lender risk and can make approval more likely at lower credit scores. You can always request a credit line increase later once your score improves. Starting smaller also reduces your minimum draw requirements and may eliminate appraisal requirements at some lenders who use automated valuation for smaller lines.

Use Your Bank or Credit Union Where You Have History

If you have had a long-standing relationship with a bank or credit union — checking account, savings, prior loans — that institution is more likely to approve your HELOC even with a lower score than the published minimum. Existing customers have demonstrated reliability through account behavior that the underwriter can see. Your existing financial institution should always be on your shortlist when applying with marginal credit.

How to Improve Your Credit Score Before Applying for a HELOC

The fastest credit score improvements before a HELOC application come from: paying down credit card balances to below 30% utilization — which can boost scores in one to two billing cycles; disputing errors on your credit report at AnnualCreditReport.com — corrected errors can lift scores within 30 to 45 days; becoming an authorized user on a long-standing account with low utilization; and avoiding new credit applications for at least 60 days before applying.

Here is a practical timeline for HELOC credit preparation:

| Timeline | Action | Expected Score Impact |

|---|---|---|

| Immediately | Pull all 3 credit reports at AnnualCreditReport.com — check for errors, outdated items, paid medical collections still showing | Dispute resolution: +10 to +50 points within 30–60 days |

| 30–45 days | Pay down credit card balances to below 30% utilization on all cards — then push toward 10% | +15 to +40 points per billing cycle |

| 60–90 days | Make every payment on time — zero late payments. Set up autopay for minimums on all accounts | Builds consistent positive history — prevents score drops |

| 60 days before applying | Stop all new credit applications — no new cards, loans, or financing. Hard inquiries hurt at HELOC application time | Prevents -5 to -15 point drops per inquiry |

| 30 days before applying | Pay balances to their lowest point — your score reflects balances as of your statement closing date | Maximum utilization reduction benefit right before scoring |

See How Far You Are From the Best HELOC Rate Tier

Use our free Credit Score Estimator to get your estimated FICO range in 30 seconds — and our Score Impact Simulator to see which actions will push you into the 700+ tier fastest.

Frequently Asked Questions

What credit score do you need for a HELOC in 2026?

Most lenders look for a minimum credit score between 620 and 680 for a HELOC, though some will go lower if you have strong equity or income. Scores of 700 or higher unlock the best rates, and even a small rate difference adds up over time. Only 4.6% of HELOCs go to borrowers below 620, making the practical floor closer to 640 at most institutions.

What is the current HELOC interest rate in June 2026?

The national average HELOC interest rate is 7.43% as of June 3, 2026, according to Bankrate’s latest survey of the nation’s largest home equity lenders. Curinos puts the national average monthly HELOC adjustable rate at 7.21% as of the same period. Rates are based on strong-credit borrowers with low CLTV ratios — borrowers with 620–660 scores can expect rates of 9% to 10% or higher.

How much home equity do you need for a HELOC?

Most home equity line of credit lenders have a minimum home equity requirement of 15% or more. This means your combined loan-to-value (CLTV) — your existing mortgage plus the HELOC — cannot exceed 85% of your home’s value. Most lenders typically allow homeowners to borrow up to 80% or 85% of their home’s value, minus the outstanding mortgage balance.

Can I get a HELOC with a 620 credit score?

Yes, but options are limited and rates will be meaningfully higher. You can get a home equity loan with a credit score of 620, but your options will be more limited and your interest rate will be higher than for people with better credit. You need to make up for it by being strong in other areas: strong income, low DTI below 36%, a lot of home equity above 20%, and a clean payment history for the last 12 to 24 months. Credit unions and online lenders are the most flexible options at this score.

What is the maximum HELOC amount I can borrow?

Most lenders typically allow homeowners to borrow up to 80% or 85% of their home’s value, minus the outstanding mortgage balance. For example: if your home is worth $400,000 and you owe $200,000 on your mortgage, at 85% CLTV your maximum HELOC is $140,000. Your credit score, income, and DTI also affect the actual credit line amount offered — lenders may approve a smaller line than the maximum for lower-credit borrowers.

Is a HELOC or cash-out refinance better in 2026?

For most homeowners with a low existing mortgage rate below 5%, a HELOC is better in 2026. For homeowners with low primary mortgage rates and a chunk of equity in their house, it is probably one of the best times to get a HELOC or a home equity loan. You do not give up that great mortgage rate, and you can use the cash drawn from your equity for things like home improvements, repairs, and upgrades. A cash-out refinance makes more sense only if your current mortgage rate is already above 6.5% and you need a large lump sum at a fixed rate.

How long does it take to get a HELOC in 2026?

A standard HELOC takes 2 to 6 weeks from application to funding. This includes the application review, home appraisal or automated valuation, title search, and closing. Some online lenders advertise closing in 5 to 7 business days for well-qualified borrowers with strong equity. Gathering documents in advance — two years of tax returns and W-2s, recent pay stubs, your current mortgage statement, and property tax bills — can significantly speed up the underwriting process.

Related Free Tools

Related Guides

- Bankrate — Current HELOC Rates, June 3, 2026

- Yahoo Finance/Curinos — HELOC Rates Today, June 3, 2026

- LendingTree — HELOC Requirements: Credit Score, Equity and Income, March 2026

- The Mortgage Reports — What Credit Score Do You Need for a HELOC in 2026?

- RefiGuide — HELOC Credit Score Requirements 2026, April 2026

- AmeriSave — 7 Critical Steps to Getting a HELOC with Bad Credit in 2026

- AmeriSave — 7 HELOC Requirements You Must Meet in 2026

- HonestCasa — HELOC Credit Score Requirements 2026, February 2026

- Freedom Mortgage — HELOC Requirements

- LendingTree — HELOC Rates, April 2026

3 thoughts on “HELOC Credit Score Requirements 2026 — What Score You Need, Current Rates, and How to Qualify”