Subprime Credit Score in 2026: Best Path to Recovery

A subprime credit score — below 620 under FICO classification — is not a life sentence. It is a starting point. Subprime borrowers in 2026 are more common than at any point since before the pandemic — driven by student loan delinquencies, rising credit card balances, and economic pressure on lower-income households. But recovery is faster than most people realize with the right strategy. This guide gives you the exact path from subprime to prime credit — the fastest actions ordered by impact, realistic timelines for each milestone, and every tool available in 2026 to accelerate your recovery.

Subprime status is not a character flaw. It is a credit profile that reflects a combination of past financial events — some within your control and some not. Medical emergencies, job loss, student loan repayment chaos, a divorce, an identity theft event — all of these can produce a subprime score from a person who is fundamentally financially responsible.

What matters more than how you got here is what you do next. And in 2026, the tools available for subprime recovery are more accessible, more effective, and more clearly mapped than they have ever been. Some people move from subprime to prime in 6 months. For others it takes 24 months. The difference is almost entirely strategy — not luck.

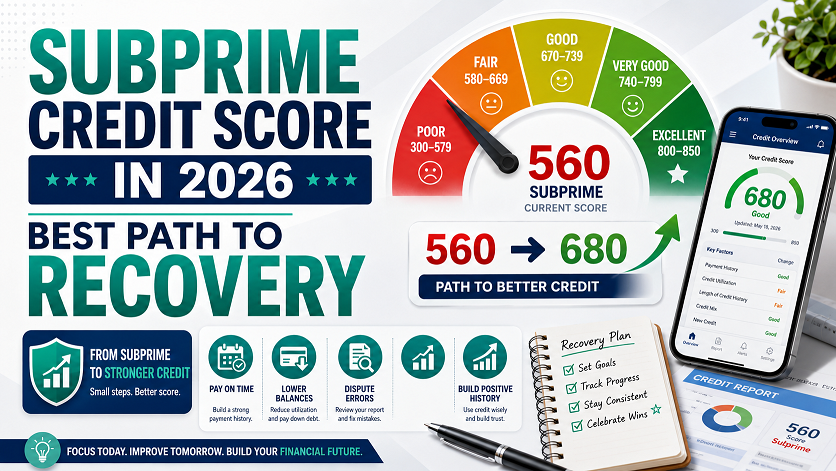

What Is a Subprime Credit Score in 2026?

The credit industry uses several tiers to classify borrowers by risk. Here is the full spectrum under the most widely used FICO classification:

In this guide, “subprime” refers to scores below 620 — covering both deep subprime (300–499) and the traditional subprime range (500–619). The 620 threshold is the most important milestone for most borrowers because it is the technical minimum for conventional mortgage loans and the entry point for most mainstream credit products.

VantageScore Defines Subprime Differently

Under VantageScore classification, the equivalent of subprime is approximately below 601. VantageScore 4.0 — now approved for Fannie Mae, Freddie Mac, and FHA mortgage underwriting — may generate a higher score than Classic FICO for subprime borrowers, particularly those with medical collections (which VantageScore ignores) or reported rent and utility history. Always check your VantageScore via Credit Karma alongside your FICO Score — a significant gap between the two is valuable information for choosing the right lender. See our full guide: VantageScore 4.0 and Your Credit in 2026.

Why More Americans Are Subprime in 2026

The percentage of Americans with subprime scores fell to historic lows during the pandemic — when stimulus payments, forbearance programs, and reduced spending pushed scores up across the board. That protective environment has fully unwound, and subprime rates are rising again in 2026 due to several specific, identifiable causes:

- Student loan delinquencies — the end of the federal on-ramp in October 2024 sent millions of missed payments to credit bureaus simultaneously, driving many near-prime borrowers into subprime territory. Full details: Student Loans and Your Credit Score in 2026

- Rising credit card utilization — inflation squeezed household budgets and pushed balances higher relative to credit limits, crossing the 30% and 50% thresholds that significantly damage scores

- Medical debt collections — despite the bureaus’ 2023 voluntary removal of sub-$500 collections and paid collections, unpaid medical debt above $500 still shows on reports and still hurts scores under Classic FICO

- Severe mortgage delinquency rising — subprime mortgage borrowers are experiencing the steepest delinquency increases of any segment, with 90+ day delinquencies climbing in 2026

- BNPL missed payments now reporting — Buy Now Pay Later providers increasingly report to bureaus, and missed installment payments are appearing as negatives for consumers who did not realize their BNPL activity was being reported

What a Subprime Score Actually Costs You — In Real Dollars

| Product | Subprime (580) Terms | Prime (720) Terms | Annual Cost Difference |

|---|---|---|---|

| Auto Loan ($30,000, 60 months) | ~16%–20% APR — $730/mo | ~6%–7% APR — $594/mo | ~$1,600+/yr more |

| Personal Loan ($10,000) | 25%–35% APR — if approved | 9%–13% APR | $1,600–$2,200/yr more |

| Credit Card APR | 28%–36% APR — secured only | 18%–22% APR — unsecured | $800–$1,400/yr on $5K balance |

| Mortgage ($300,000, 30yr) | FHA at ~7.5%–8% — $2,100+/mo | Conventional at ~6.5% — $1,896/mo | $2,400+/yr — $72,000+ over loan life |

| Apartment rental | Higher security deposit or denial | Standard deposit, more options | $500–$2,000 extra upfront deposit |

Subprime Status Can Cost $5,000 to $8,000 More Per Year in Interest Alone

A borrower with a 580 score who has an auto loan, a credit card balance, and a personal loan is paying an estimated $5,000 to $8,000 more per year in interest than a borrower with a 720 score carrying the same debt amounts. Over five years, that is $25,000 to $40,000 in additional interest — money that could have gone toward savings, investments, or a down payment. Improving from subprime to prime is not just a number improvement — it is one of the highest-ROI financial actions available to a subprime borrower in 2026.

Step 1 — Diagnose Your Specific Situation

Before taking any action, you need to know exactly why your score is subprime. The cause determines the fastest fix. Pull your free reports at AnnualCreditReport.com from all three bureaus and identify which of these categories applies to your situation:

| Primary Cause | Fastest Fix Available | Time to Impact |

|---|---|---|

| High credit card utilization (above 50%) | Pay balances below 10% — fastest action available | 30 days |

| Errors on your credit report | Dispute with each bureau — removes negative item | 30–45 days |

| Medical collections under $500 or paid | Dispute as should-have-been-removed per 2023 bureau policy | 30–45 days |

| Collection accounts — unpaid | Negotiate pay-for-delete before paying | 30–90 days if successful |

| Student loan delinquency | Enroll in IDR immediately — stop new damage | Stops damage now; recovery 12–24 months |

| Late payments — recent | Pay current, attempt goodwill removal letter | Impact fades over 12–24 months of clean history |

| Thin file — too few accounts | Add secured card + credit builder loan + Experian Boost | 3–6 months for meaningful improvement |

| Bankruptcy — recent | Rebuild with secured card + authorized user strategy | 12–24 months to reach 620; 2–3 years to reach 680+ |

Step 2 — The Fastest Score Wins Available Right Now

These are the actions that can produce score improvement within 30 to 60 days — before you even begin the longer-term rebuilding strategies:

If high utilization is contributing to your subprime score, this is your single highest-priority action. Credit utilization accounts for 30% of your Classic FICO score. Moving from 80% utilization to under 10% can add 30 to 70 points in a single billing cycle. Even if you cannot pay everything down, focus on getting at least one card to under 30% — every account that crosses a utilization threshold downward helps. Use our utilization calculator to find your exact target paydown amount.

For subprime borrowers, error disputes are among the most high-value actions available. Common removable items: paid medical collections (should be removed per 2023 bureau policy), unpaid medical collections under $500 (should be removed), any item past its 7-year reporting window (must be removed under FCRA), accounts you do not recognize (possible identity theft or error), and incorrect payment statuses. File disputes online at Equifax.com, Experian.com, and TransUnion.com simultaneously. Bureaus must investigate within 30 days. Removing a single collection account can add 40 to 100 points. Full guide: Medical Debt and Credit Reports 2026.

Experian Boost adds your utility, phone, streaming, and other recurring bill payments to your Experian credit file — for free, immediately. For subprime borrowers with thin files or few positive accounts, this can add meaningful positive payment history. The average improvement is 13 points on Experian FICO Score 8, with larger improvements common for thin-file consumers. It only affects your Experian score, but since lenders often pull all three, even improving one bureau’s score can matter. Go to Experian.com, create a free account, and connect your bank account. Full guide: Does Paying Utilities Build Credit in 2026?

Before paying any collection account, contact the collection agency and negotiate a pay-for-delete agreement — a written agreement that the agency will remove the tradeline from your credit report in exchange for payment. Not all collection agencies will agree to this, but many will — especially for older debts or partial payment offers. Get the agreement in writing before paying a single dollar. Under Classic FICO 8, a paid collection that remains on your report still counts as a negative mark and does not significantly improve your score. Under a pay-for-delete agreement, the entire tradeline disappears — which can add 50 to 100+ points immediately upon removal. See our pay-for-delete letter templates for exact wording.

Step 3 — The Building Blocks for Sustained Recovery

After addressing the fastest wins, the next phase is adding positive accounts and building consistent payment history. These actions take 3 to 12 months to show their full impact but are essential for reaching and maintaining prime credit status.

A secured credit card is the most accessible credit-building tool for subprime borrowers. You deposit $200 to $500 as collateral — that amount becomes your credit limit. The card reports to all three bureaus as a regular revolving account. Use it for one or two small recurring purchases each month — a streaming subscription, a phone bill — and pay the full balance every single month. Keep the balance below 10% of the limit at statement close date. After 12 months of on-time payments, many secured card issuers will upgrade you to an unsecured card and return your deposit.

A credit builder loan adds an installment account to your credit file — diversifying your credit mix (a scoring factor) and building 12 months of positive installment payment history. You make monthly payments; the money is held in a savings account and released at the end of the term. Self is the most widely available option at approximately $25 per month. Many credit unions offer credit builder loans to members with lower fees. The combination of a secured card (revolving) and a credit builder loan (installment) gives you both account types that scoring models reward — and 12 months of consistent on-time payments across both significantly moves a subprime score.

If a family member or trusted friend has a credit card that is at least 2 to 3 years old with low utilization and no late payments, ask to be added as an authorized user. The entire history of that card can appear on your credit report within one billing cycle — instantly adding years of positive payment history, increasing your average account age, and improving your utilization ratio if the card carries a low balance. You do not need to use the card. The account holder’s positive behavior benefits you; their negative behavior also affects you, so choose the account carefully.

If you have been paying rent consistently, enroll in Rental Kharma or Rock the Score to add up to 24 months of past rent payments to your TransUnion and Equifax files. This adds a full rental tradeline with up to two years of positive payment history — one of the fastest ways to add substantial positive history to a subprime file. Under VantageScore 4.0, this rent history factors directly into your mortgage score. Even under Classic FICO, the additional positive tradeline helps reduce the proportional weight of negative items. Full guide: How to Get Credit for Paying Rent in 2026.

Best Secured Credit Cards for Subprime Recovery in 2026

Not all secured cards are equal. These are the best options specifically for subprime recovery — all report to all three bureaus and have clear upgrade paths:

Avoid Secured Cards With High Annual Fees and No Upgrade Path

Some secured cards marketed to subprime borrowers charge $75 to $100+ in annual fees, have high APRs (which matters if you ever carry a balance), and have no path to upgrade to an unsecured card. These are designed to profit from subprime borrowers rather than help them recover. Always check: (1) Does it report to all 3 bureaus? (2) What is the annual fee? (3) Is there an automatic upgrade review? If the answer to any of these is unclear or unfavorable, choose a different card. The Discover it Secured and Capital One Platinum Secured are the two safest choices for most subprime borrowers in 2026.

Score Milestones — What Each Threshold Unlocks

Recovery is not a single destination — it is a series of milestones, each unlocking new financial options. Here is what each threshold means for your real-world access to credit:

At 580, you qualify for an FHA mortgage with 3.5% down — the first path to homeownership from subprime territory. Rates will be high and MIP lasts the life of the loan, but the door is open. Also: some credit unions will approve secured personal loans and auto loans at 580.

Crossing 620 is the most important milestone for most subprime borrowers. Conventional mortgages become technically available. Most auto lenders offer significantly better rates. More unsecured personal loan options appear. Credit card offers improve noticeably. This is the primary target for most subprime recovery plans.

At 660, auto loan rates improve significantly. Credit card issuers begin offering unsecured cards with real credit limits. Apartment rental applications become much easier. Lender overlays on conventional mortgages begin to open up. Personal loan APRs drop into the 15%–20% range from 25%+.

At 700, you have access to virtually all mainstream credit products. Auto loan rates drop into competitive territory. Credit cards with real rewards programs become available. Mortgage rates improve materially. Most lender overlays are no longer a barrier. This is the target for borrowers planning to apply for a mortgage in the next 12 months.

At 740+, you qualify for the best rate tier on mortgages, auto loans, and personal loans. Premium credit card offers with best-in-class rewards become available. HELOC approval at best margins. This is the long-term target — typically 18 to 36 months from a subprime starting point with consistent strategy execution.

Your 12-Month Subprime Recovery Plan

Here is a concrete month-by-month plan combining all the strategies above. Adapt it based on your specific situation — not every step applies to every borrower:

Pull all 3 reports. Activate Experian Boost (free). Pay down card balances below 30%. File disputes for all errors and should-be-removed items. Contact any collection agencies about pay-for-delete. Check VantageScore vs FICO gap.

Apply for secured credit card (Discover it Secured or Capital One). Enroll in rent reporting with Rental Kharma or Rock the Score — submit 12–24 months of bank statements. Ask trusted family member about authorized user status.

Enroll in Self credit builder loan (~$25/mo). Dispute outcomes start arriving — track removals and score changes. First secured card statement arrives — pay in full. Rent tradeline beginning to appear on reports.

Consistent on-time payments on all accounts. Pay down remaining card balances to under 10%. Goodwill letters for any recent late payments. Many subprime borrowers reach 580–620 at this stage if they started around 500–550.

Check for secured card upgrade eligibility (Discover auto-reviews at 7 months). Continue credit builder loan payments. Older negative marks losing impact with each month of clean history. Target: 600–640 range for borrowers starting at 500.

Most borrowers who follow this plan reach 620+ by month 12. Some reach 640–660. Review all accounts. Credit builder loan nearing completion. Consider applying for an unsecured card if secured card has been upgraded. Set 740 as next milestone.

The One Rule That Overrides Everything Else

Every strategy in this guide produces results only if you make every single payment on time going forward. Payment history is 35% of your FICO score — the largest single factor. One missed payment during your recovery period can erase months of progress. Set up autopay for at least the minimum on every account, every month. Then pay more than the minimum when you can. But never, under any circumstances, miss a payment during your recovery window. The accounts you open for recovery become liabilities if you miss payments on them.

See Your Personalized Recovery Timeline

Use our free Credit Rebuild Timeline — enter your current score, negative items, and target score to see exactly when you will cross 580, 620, 660, and 700 milestones.

Frequently Asked Questions

What is considered a subprime credit score in 2026?

A subprime credit score is generally defined as a FICO score below 620. Deep subprime is typically 300–499, and standard subprime is 500–619. Under VantageScore, the equivalent is approximately below 601. Approximately 16% of U.S. consumers fall in the subprime range as of 2026, with the share trending upward from the pandemic-era low due to student loan delinquencies, rising card utilization, and economic pressure on lower-income households.

How long does it take to recover from a subprime credit score?

Recovery time depends on the cause. High utilization can improve in 30 to 60 days once balances are paid down. Errors disputed and removed improve scores within 30 to 45 days. For scores driven by collection accounts and late payments, reaching 620 typically takes 12 to 24 months of consistent positive behavior. Borrowers who combine multiple strategies simultaneously — utilization reduction, error disputes, secured card, credit builder loan, rent reporting — consistently recover faster than those using a single approach.

What credit cards can I get with a subprime credit score?

Your primary options are secured credit cards. The best for subprime recovery in 2026 are Discover it Secured (no annual fee, all 3 bureaus, automatic upgrade review at 7 months) and Capital One Platinum Secured (low minimum deposit options, all 3 bureaus, upgrade path). Chime Credit Builder requires no hard inquiry and is a good option if you already use Chime. Avoid secured cards with high annual fees and no upgrade path — they are designed to profit from subprime borrowers rather than help them recover.

Can I buy a house with a subprime credit score in 2026?

At 580 or above, FHA loans are available with 3.5% down. Below 580, FHA requires 10% down. VA loans have no official minimum for eligible veterans. However, rates at 580 to 619 are significantly higher than at 640+, and combined with FHA mortgage insurance, the monthly cost is substantially more. Most advisors recommend reaching at least 620 before applying, and 680 for materially better rates. A few months of recovery work often saves tens of thousands over the loan term.

Does paying off collections improve a subprime credit score?

It depends. Under Classic FICO 8, paying a collection does not remove it and may not improve your score — the paid collection still shows as negative. Under FICO 9 and VantageScore 4.0, paid collections carry less weight. The best strategy: negotiate a pay-for-delete agreement in writing before paying. If the agency removes the tradeline upon payment, your score improves under all models. Without pay-for-delete, benefit is model-dependent. Never pay a collection without first requesting debt validation and attempting a pay-for-delete negotiation.

What is a credit builder loan and does it work for subprime recovery?

A credit builder loan holds your payments in a savings account and reports them to credit bureaus as installment loan payments. You receive the money at the end of the loan term. For subprime borrowers, it adds an installment account to the credit mix and builds 12 months of positive payment history — both significant scoring factors. Self is the most widely available option at ~$25/month. Most credit unions also offer credit builder loans. Combining a secured card (revolving) with a credit builder loan (installment) is one of the most effective two-account subprime recovery strategies available.

How does the authorized user strategy work for subprime credit recovery?

Being added as an authorized user on a trusted person’s credit card can instantly add that account’s full history to your credit report — potentially adding years of positive payment history, a longer average account age, and better utilization in one billing cycle. Choose an account with at least 2 to 3 years of history, zero late payments, and utilization below 30%. The account holder’s negative behavior also affects you, so choose carefully. This is one of the fastest 30 to 60 point improvements available to subprime borrowers at no direct cost.

Related Guides

Related Free Tools

- CFPB — Consumer Credit Trends Data

- Experian — Average Credit Score in America and Score Distribution

- FICO — Credit Score Ranges and Classification

- Equifax — April 2026 Consumer Pulse: Latest Consumer Credit Trends

- Federal Reserve — Consumer and Community Context: Credit Access

- VantageScore — VantageScore 4.0 Fact Sheet

- Self — Credit Builder Loan Product