HELOC vs Cash-Out Refinance: Credit Score Requirements Compared 2026

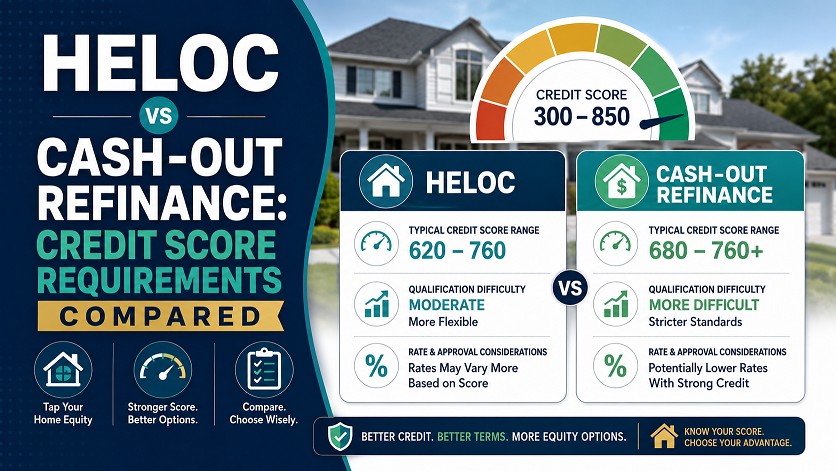

Both HELOCs and cash-out refinances require a minimum credit score of 620 for conventional programs in 2026 — with FHA cash-out available at 580 and VA cash-out available to eligible veterans with flexible score minimums. The minimum score is similar for both products. What differs dramatically is which product makes more financial sense at each score level, how each product affects your credit score going forward, and — most importantly in 2026 — what happens to your existing mortgage rate. This guide compares both products head-to-head across every relevant dimension so you can make the right decision for your situation.

The decision between a HELOC and a cash-out refinance is one of the most consequential financial choices a homeowner can make — and in 2026, the answer is clearer for most borrowers than it has been in years. The reason: most American homeowners locked in mortgage rates between 2.75% and 4.5% in 2020 and 2021, and those rates are still dramatically lower than today’s refinance rates.

For those borrowers, a cash-out refinance is not just a question of accessing equity — it is a question of whether giving up a generational mortgage rate to do so is worth it. In most cases in 2026, it is not. But the answer is not the same for everyone, and understanding the credit score requirements, rate structures, and total costs for each product gives you the information to make the right call.

Product Overview — What Each One Is

- Second loan added on top of existing mortgage

- Revolving credit line — draw what you need, when you need it

- Variable interest rate — tied to prime rate plus margin

- Your first mortgage rate is completely untouched

- Interest-only payments during draw period (typically 10 years)

- Lower closing costs — typically $500 to $2,000

- HELOC balance counts as revolving utilization on credit report

- Faster approval — typically 2 to 4 weeks

- Replaces your existing mortgage entirely with a new, larger loan

- Lump sum payment at closing — fixed amount

- Fixed interest rate option available — predictable payment

- Your existing mortgage rate is replaced by today’s rate

- Full principal + interest payments from day one

- Higher closing costs — typically 2% to 5% of new loan amount

- New mortgage installment account on credit report

- Slower approval — typically 30 to 60 days

Credit Score Requirements — Side by Side

Key Difference: FHA and VA Are Only Available for Cash-Out Refinance

There is no FHA HELOC and no VA HELOC. If your credit score is below 620 and you want to access home equity, a cash-out refinance via FHA (580+ minimum) or VA (no official minimum) is your only mainstream option. For borrowers with scores between 580 and 619, an FHA cash-out refinance is the only realistic path to equity access through a mainstream lender. This is a significant difference — HELOCs are only available through conventional programs, which require 620 as the practical floor.

Which Product Is Better at Each Score Tier

How Rates Compare — HELOC vs Cash-Out Refi in 2026

Rates for both products in 2026 are driven by different benchmarks — and understanding the difference helps you evaluate which is cheaper for your specific situation.

| Factor | HELOC Rate Structure | Cash-Out Refi Rate Structure |

|---|---|---|

| Rate benchmark | Prime rate (currently ~7.5%) + margin | 10-year Treasury yield + spread |

| Rate type | Variable — changes with prime rate | Fixed available — predictable for life of loan |

| Score 740+ rate (est. June 2026) | ~7.75%–8.25% | ~6.5%–7.0% on new loan |

| Score 620 rate (est. June 2026) | ~9.0%–10.0% | ~7.5%–8.0% on new loan |

| Rate risk | Rising prime rate raises your payment | Fixed rate — immune to rate increases |

| Rate applies to | Only the drawn HELOC balance | Entire new mortgage balance including existing loan |

Cash-Out Refi Has a Lower Rate — But That Rate Applies to Your Entire Mortgage

A cash-out refinance rate in 2026 looks lower than a HELOC rate on the surface. But this comparison is misleading. The cash-out refi rate applies to your entire new mortgage balance — including the portion that was your existing mortgage. If you have a $400,000 mortgage at 3.5% and refinance to access $75,000 in equity, you now have a $475,000 mortgage at 7.0%. Your interest on the original $400,000 goes from ~$14,000 per year to ~$28,000 per year — an increase of $14,000 annually just to access $75,000. The HELOC charges a higher rate but only on the $75,000 you drew — costing perhaps $6,000 to $7,500 per year on that amount while leaving your existing $400,000 at 3.5%.

Total Cost Comparison on a $100,000 Equity Draw

Here is a concrete side-by-side cost comparison for a borrower who wants to access $100,000 in equity and has an existing mortgage of $350,000 at 3.5%:

| Cost Element | HELOC ($100K draw, 740+ score) | Cash-Out Refi ($100K drawn, 740+ score) |

|---|---|---|

| Closing costs | ~$1,000–$2,000 | ~$9,000–$15,000 (2%–3% of $450K loan) |

| Rate on the $100K | ~8.25% (variable) | ~6.75% (fixed) |

| Annual interest on $100K | ~$8,250 | ~$6,750 (on this portion only) |

| Extra annual cost on existing $350K | $0 — existing rate untouched at 3.5% | +~$11,900/yr (rate rises from 3.5% to 6.75%) |

| Total extra annual cost | ~$8,250/yr (HELOC interest only) | ~$18,650/yr (refi adds $6,750 + $11,900) |

| Break-even on closing costs | N/A — low upfront cost | Never — ongoing cost exceeds HELOC by ~$10,400/yr |

For Most 2026 Homeowners, a Cash-Out Refi Costs $10,000+ More Per Year Than a HELOC

For a borrower with an existing mortgage at 3.5% who wants to access $100,000 in equity, the cash-out refinance option costs approximately $10,000 to $15,000 more per year than a HELOC — because the cash-out refi reprices the entire existing mortgage at today’s higher rates. This is the defining financial reality of the 2026 housing market. Unless your existing mortgage rate is already above 6%, the math almost always favors a HELOC over a cash-out refinance for accessing equity in 2026.

How Each Product Affects Your Credit Score

The two products have different effects on your credit score — both at the time of application and over time. Understanding this helps you plan if you have other credit needs in the near term.

| Credit Impact | HELOC | Cash-Out Refinance |

|---|---|---|

| Hard inquiry at application | Yes — 5 to 10 pt temporary drop | Yes — 5 to 10 pt temporary drop |

| Account type added | Revolving account (like a credit card) | New installment account (mortgage) |

| Effect on credit utilization | Drawing on HELOC increases revolving utilization — can drop score significantly if large draws | No revolving utilization impact — installment loan |

| Effect on account age | New account lowers average age slightly | New account + old mortgage closed — can reduce average age more |

| Long-term score impact | Neutral to positive with on-time payments; negative if high utilization | Neutral to positive — large installment loan with on-time payments builds strong history |

| Recovery time | 12–24 months to fully recover from initial impact | 12–24 months to fully recover from initial impact |

HELOC Utilization Is a Hidden Score Risk — Keep Draws Below 30%

The most underappreciated credit score risk of a HELOC is utilization. A $100,000 HELOC that you draw $80,000 from is reported to the bureaus as 80% utilization on a revolving account. This can drop your score by 30 to 50 points — exactly the same way running up a credit card to 80% of its limit would. Best practice: keep your total HELOC draw below 30% of the credit line at any given time, or if you need a large amount, consider drawing it in stages rather than all at once. A cash-out refinance has no utilization impact — the borrowed amount is an installment loan, not a revolving balance.

The Most Important Factor — Your Existing Mortgage Rate

No comparison of HELOC vs cash-out refinance in 2026 is complete without this framework. Your existing mortgage rate is the single most important variable in the decision:

| Your Existing Mortgage Rate | Recommended Product | Reason |

|---|---|---|

| Below 4.0% (locked in 2020–2021) | HELOC — strongly preferred | Giving up a sub-4% rate for a 6.5%–7% refi rate is extremely costly |

| 4.0%–5.0% | HELOC — generally preferred | Still a meaningful rate gap — HELOC preserves the favorable first mortgage rate |

| 5.0%–6.0% | Case by case — calculate both | Gap is narrowing — run the full cost comparison for your specific numbers |

| 6.0%–6.5% | HELOC still often better | Cash-out refi rate only slightly above existing — but closing costs still favor HELOC |

| Above 6.5% | Cash-out refi worth considering | If you can significantly reduce your first mortgage rate via refi, the math changes |

| Above 7.5% (bought at market peak) | Cash-out refi — strongly consider | A cash-out refi at 6.5%–7% saves money on the first mortgage AND accesses equity |

Best Scenarios for Each Product

- Your existing mortgage rate is below 5.5%

- You want flexibility to draw only what you need

- You are funding a home renovation in stages

- You want lower closing costs

- You need faster access to funds (2–4 weeks)

- You plan to repay the balance within a few years

- You want to keep your first mortgage untouched

- Your credit score is 680+ for best HELOC rates

- Your existing mortgage rate is above 6.5%

- You want a fixed rate on the full amount accessed

- You need a large lump sum and will use all of it

- Your score is 580–619 (FHA cash-out available; no FHA HELOC)

- You are VA-eligible (no VA HELOC; VA cash-out available)

- You want to consolidate your first mortgage and equity access into one payment

- Current rates are significantly below your existing rate

How to Improve Your Score for Either Product

Whether you are targeting a HELOC or a cash-out refinance, the score improvement strategies are the same — and the thresholds that matter are identical. Here are the key actions:

Pay Down Credit Card Balances to Under 10% Utilization

Both products use the middle score from all three bureaus. Reducing credit card utilization is the single fastest score improvement available — results typically appear within one billing cycle (30 days). Target under 10% on each card individually, not just in aggregate. On a $300,000 home equity product, even a 20-point score improvement can save hundreds of dollars per year in rate margin.

Dispute Errors and Remove Medical Collections

Medical collections under $500 should already be removed under the bureaus’ 2023 voluntary policy. Any paid collection should also be removed. Any item past its 7-year reporting window must be removed under FCRA. Dispute all of these with the relevant bureau immediately. For borrowers near a score threshold — say 715 trying to reach 740 — removing a single erroneously reported collection can make the difference between the Good rate tier and the Very Good rate tier. Full details: Medical Debt Credit Report 2026 and Dispute Guide 2026.

Check Your VantageScore 4.0 — It May Be Higher Than Your FICO

Both HELOCs and cash-out refinances can now be underwritten using VantageScore 4.0, which ignores medical collections and factors in rent and utility history. Check your VantageScore via Credit Karma and compare it to your FICO Score 8 via Experian. If your VantageScore is meaningfully higher — which is common for consumers with medical collections — specifically seek out lenders who use VantageScore 4.0 for underwriting. For HELOC or cash-out refi applicants near the 680 or 740 threshold, the right scoring model choice can be the difference between rate tiers. See: VantageScore 4.0 Guide.

Make All Payments on Time — Especially Your First Mortgage

Both HELOC and cash-out refi lenders scrutinize your first mortgage payment history intensely. Any late payment on your first mortgage in the past 12 to 24 months is a significant red flag for both products. In the months before applying for either product, make every mortgage payment on time without exception. For other accounts, set up autopay for at least the minimum on all credit cards and loans. Consistent on-time payment history compounds over time and is the strongest long-term score builder available.

See Where Your Score Stands for Both Products

Use our free Credit Score Estimator — check your estimated FICO range and see how close you are to the 680 and 740 rate thresholds for both HELOCs and cash-out refinances.

Frequently Asked Questions

What credit score do you need for a cash-out refinance in 2026?

For a conventional cash-out refinance, most lenders require a minimum of 620, though many apply overlays requiring 640 to 680. FHA cash-out refinance is available at 580 minimum. VA cash-out refinance has no official minimum but most lenders want 580 to 620. For the best rates and lowest loan-level price adjustments, you need 740 or above. Between 620 and 680, you qualify but pay a meaningful rate premium.

Is a HELOC or cash-out refinance better in 2026?

For most homeowners in 2026 with an existing mortgage rate below 5.5%, a HELOC is the better choice. A cash-out refinance replaces your entire mortgage at today’s higher rates — potentially adding thousands of dollars per month in first mortgage cost even if you only want a fraction of your equity. A HELOC accesses equity without touching your existing rate. The exception: if your existing mortgage rate is already above 6.5%, a cash-out refinance may make sense.

Can I do a cash-out refinance with a 620 credit score?

Yes. Conventional cash-out refinances are available at 620, though many lenders require 640 or higher. FHA cash-out refinances are available at 580. VA cash-out refinances are available to eligible veterans with flexible score requirements. At 620, loan-level price adjustments will increase your effective rate by 0.75% to 1.5%. Combined with replacing a low existing mortgage rate, the total cost at 620 can be very high — calculate the full picture before proceeding.

Which has lower credit score requirements — HELOC or cash-out refinance?

Both have similar conventional minimums at 620. The key difference: FHA cash-out refinance is available at 580 with no equivalent FHA HELOC, and VA cash-out refinance offers the most flexible score requirements with no official minimum. For borrowers between 580 and 619, FHA or VA cash-out refinance are the only mainstream options for accessing home equity — HELOCs are not available below 620.

How does a cash-out refinance affect your credit score?

A cash-out refinance generates a hard inquiry (5 to 10 point drop), creates a new mortgage account (reduces average account age), and closes your old mortgage. Most effects are temporary — within 12 to 24 months, consistent on-time payments restore any lost points. The long-term effect is neutral to positive. There is no revolving utilization impact since it is an installment loan.

How does a HELOC affect your credit score?

A HELOC generates a hard inquiry (5 to 10 point drop) and creates a new revolving account. The most important ongoing impact: drawing heavily on a HELOC increases your revolving utilization — using $80,000 of a $100,000 HELOC shows 80% utilization and can drop your score 30 to 50 points. Keep HELOC draws below 30% of the credit line to minimize utilization impact. Unlike a cash-out refi, the HELOC’s score impact is directly tied to how much of the line you use.

What LTV ratio is required for a cash-out refinance in 2026?

Most lenders cap conventional cash-out refinances at 80% LTV — you must retain at least 20% equity after the refinance. FHA cash-out refinances also cap at 80% LTV. VA cash-out refinances can go up to 90% LTV in some cases. At lower credit scores (620 to 660), some lenders require lower LTV — 70% to 75% — as a compensating factor. Higher equity (lower LTV) consistently unlocks better rates regardless of credit score.

Related Guides

Related Free Tools

- Fannie Mae — Credit Score and LTV Requirements for Cash-Out Refinance

- Freddie Mac — Origination and Underwriting Guidelines

- HUD — FHA Cash-Out Refinance Requirements

- CFPB — Home Equity Lines of Credit (HELOC)

- Bankrate — Current HELOC and Cash-Out Refinance Rates

- VA — Cash-Out Refinance Loan Program

- Equifax — April 2026 Consumer Pulse: Latest Consumer Credit Trends