Auto Loan Credit Score Requirements 2026 — Rates by Credit Tier, Minimum Scores, and How to Get the Best Deal

There is no universal minimum credit score for an auto loan in 2026 — but your score determines your rate tier, which directly impacts your monthly payment and total interest. The current average rate for a new car loan is 6.98% (Bankrate, June 3, 2026). For new cars, super-prime borrowers (781+) see rates of 5%–6%, while subprime borrowers (501–600) face 15%+. On a $25,000 loan over 60 months, the difference between prime and subprime rates is over $5,000 in extra interest. This guide covers every credit tier, what rate you can expect, and exactly how to qualify for the best terms at your score.

In 2026, the average rate on a car loan falls around 6.5%–7% for new cars and 11%–12% for used cars. But those averages mask an enormous range depending on your credit score. A borrower with excellent credit will pay around $160 less per month than a borrower with poor credit — and may end up saving over $9,500 in interest over the life of the loan.

Car prices hit record highs in 2026, making it even more important to get the best rate on a vehicle loan. Understanding exactly which credit tier you fall into, what rate that tier commands, and what you can do to move into a better tier before you shop is the difference between an affordable car payment and one that strains your budget for years.

The 5 Auto Loan Credit Tiers — Complete 2026 Breakdown

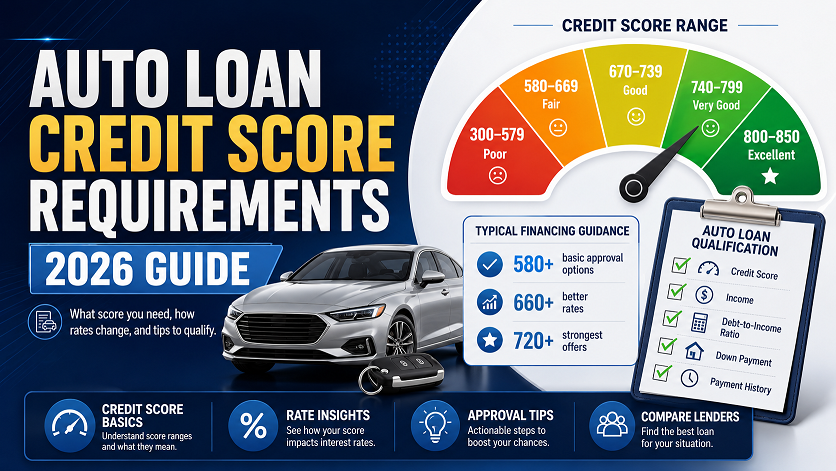

Auto lenders group borrowers into credit tiers: super prime (781+), prime (661–780), near prime (601–660), subprime (501–600), and deep subprime (500 and below). Here is what each tier means for your approval odds and rate in 2026:

Rate by Credit Score — New Car vs Used Car in 2026

Your credit score has a direct impact on your interest rate. For a new car loan in 2026: borrowers with scores above 780 can expect rates around 5% to 6%. Scores between 660 and 779 typically see rates from 6% to 9%. Fair credit scores (600 to 659) often mean rates between 10% and 14%. Subprime borrowers (below 600) may face rates of 15% or higher.

*Monthly payment based on $25,000 new car loan, 60-month term. Rate estimates sourced from Experian State of the Automotive Finance Market Q4 2025, Firstcard April 2026, Bankrate June 2026. Actual rates vary by lender and individual profile.

The Real Cost of a Lower Score — $25,000 Car Loan, 60 Months

On a $25,000 loan over 60 months, the difference between a 6% rate and a 14% rate is roughly $5,500 in extra interest. That is real money. Here is the full picture across every credit tier:

| Credit Score | Est. APR (New Car) | Monthly Payment | Total Interest | Extra vs Best Rate |

|---|---|---|---|---|

| 781–850 (Super Prime) | 5.5% | $481 | $3,860 | — Best rate |

| 720–780 (Prime High) | 6.8% | $494 | $4,640 | +$780 |

| 660–719 (Prime) | 8.5% | $513 | $5,780 | +$1,920 |

| 601–659 (Near Prime) | 11.5% | $548 | $7,880 | +$4,020 |

| 501–600 (Subprime) | 16.0% | $609 | $11,540 | +$7,680 |

| Below 500 (Deep Sub) | 21.0% | $674 | $15,440 | +$11,580 |

Moving One Tier Can Save Thousands — Not Just Hundreds

Moving from subprime (600 score) to near-prime (640 score) saves approximately $3,660 in total interest on a $25,000 car loan. Moving from near-prime (640) to prime (680) saves another $2,100. A focused 3 to 6-month credit improvement effort before buying can realistically move you one to two tiers — which on a $30,000+ vehicle purchase is the financial equivalent of negotiating thousands off the sticker price.

See What Car Loan You Qualify For at Your Score

Use our free Loan Affordability Calculator — enter your income, existing debts, and credit score to see your estimated auto loan amount and monthly payment at 2026 rates.

What Else Affects Your Auto Loan Rate Besides Credit Score

Your credit score determines your tier — but within that tier, several other factors determine your exact rate:

| Factor | How It Affects Your Rate | What to Do |

|---|---|---|

| Down payment | More down = lower LTV = lower rate. 20%+ down can improve your rate tier. | Aim for at least 10%–20% down. Even $1,000–$2,000 extra down helps. |

| Loan term | Shorter terms (36–48 mo) typically have lower rates than 72–84 mo loans. | Choose the shortest term your budget allows. 60 months is the standard sweet spot. |

| New vs used vehicle | Used car rates are typically 3%–5% higher than new car rates at every tier. | If credit is marginal, a cheaper new car may cost less overall than a used car at a higher rate. |

| Loan-to-value ratio (LTV) | Borrowing more than the car is worth increases lender risk and your rate. | Never roll in negative equity from a trade-in — it makes LTV worse and rate higher. |

| Debt-to-income ratio | High DTI limits approval odds even with decent credit. Most lenders cap at 45%–50%. | Pay down a credit card before applying to reduce monthly obligations. |

| Employment / income | Stable employment history and verifiable income significantly improve approval odds. | Have recent pay stubs and W-2 ready. Self-employed: 2 years of tax returns. |

| Lender type | Credit unions typically offer 0.5%–2% lower rates than banks or dealerships for the same borrower. | Always get a credit union pre-approval — even if you end up financing elsewhere. |

Best Lenders by Credit Score Tier — 2026

Super Prime and Prime (661+) — Best Options

- LightStream (SunTrust/Truist) — No maximum loan, rates from 6.94%+ for excellent credit, no fees, no restrictions on vehicle age or mileage

- PenFed Credit Union — Competitive rates for members, 660+ score preferred, rates from 4.74% on new cars for top-tier borrowers

- Your primary bank or credit union — Existing relationship often means preferred rates; always check your own institution first

- Manufacturer financing (e.g., Ford Credit, Toyota Financial) — Promotional rates including 0% for 781+ scores on select models

Near Prime (601–660) — Best Options

- Credit unions — Most flexible for 601–660 range; Navy Federal, PenFed, and local credit unions consistently offer 1%–3% lower rates than banks at this tier

- Capital One Auto Finance — Accepts 600+, pre-qualification available online without hard inquiry, wide dealer network

- myAutoLoan — Aggregator that sends your application to multiple lenders; minimum 600 score, rates from 6.74%, Bankrate Best for Fair Credit 2026

- Caribou — Best for refinancing; minimum 600, APR from 4.64%–28.55%, Bankrate Best for Fair Credit Refinancing

Subprime (500–600) — Best Options

- Auto Credit Express — Specialist network for credit scores as low as 500; works with subprime and deep subprime borrowers specifically

- DriveTime — In-house financing for 500+ scores; higher rates but transparent pricing and nationwide locations

- Carvana — Online purchasing with in-house financing for subprime borrowers; higher rates but convenient process

- First-time buyer programs at local dealers — Many franchise dealers have special finance departments that work with 500–580 scores

Get Pre-Approved Before You Visit the Dealership

Get pre-approved. Apply for pre-approval from your bank, credit union, or an online lender before shopping for a car. Pre-approval locks in a rate and gives you a benchmark to compare against dealer financing. Without a pre-approval, the dealership controls the financing conversation completely. With one, you have a rate floor to beat — and dealers often will beat an outside rate to keep the financing in-house.

New Car vs Used Car — Which Is Better for Lower Credit?

Counterintuitively, a new car can sometimes be the better financial choice for a borrower with fair or subprime credit. Here is why:

| Factor | New Car | Used Car |

|---|---|---|

| Interest rate | Lower — typically 3%–5% less than used | Higher — especially for subprime borrowers |

| Manufacturer incentives | Available — cash back, 0% APR for super prime | None |

| Lender availability | More lenders offer new car financing | Some lenders restrict age/mileage for subprime |

| Sticker price | Higher — averages $47,000+ in 2026 | Lower purchase price |

| Depreciation risk | Drops 15%–20% year one — risk of going upside-down | Less first-year depreciation |

| Reliability | Warranty coverage — fewer unexpected repairs | Older vehicles = more repair risk |

The Subprime New Car Trap to Avoid

Buying a new car at a 16% subprime rate on a 72-month term is one of the costliest financial decisions possible. The car depreciates 20% in year one while you owe 16% interest — creating a deep negative equity position (being “upside-down”) that can trap you for years. If you must buy at a subprime rate, choose a used car with a lower purchase price, make the largest down payment possible, and use the shortest loan term your budget allows.

Dealer Financing vs Bank vs Credit Union — Which Is Cheaper?

| Financing Source | Typical Rate Premium | Best For | Watch Out For |

|---|---|---|---|

| Credit union | Usually lowest — 0.5%–2% below banks | Anyone — especially near-prime/subprime | Must be a member; application process may take a day |

| Bank / online lender | Standard market rates | Prime and super-prime borrowers | Stricter approval at lower scores than credit unions |

| Dealership financing | Typically 1%–3% above direct lender | Convenience; manufacturer promotional rates | Dealer marks up the rate — negotiate APR separately from price |

| Buy-here-pay-here lot | Very high — 20%–30% rates common | Deep subprime with no other options | Predatory terms; vehicles often overpriced; GPS tracking common |

How to Get the Best Auto Loan Rate at Your Score — Step-by-Step

Check Your Credit Score and Reports Before Anything Else

Pull your free reports from all three bureaus at AnnualCreditReport.com before setting foot in a dealership. Know exactly which credit tier you fall into. Look for errors — incorrect late payments, paid collections still showing, accounts you do not recognize. Disputing a single significant error can add 20 to 50 points and move you into a better rate tier. Under 2026 medical debt rules, paid medical collections and unpaid medical debts under $500 should already be removed — if they are still showing, dispute them immediately before applying for any loan.

Get Pre-Approved From Multiple Lenders — All Within 14 Days

The current auto loan interest rate sits at 6.98% for a 60-month new car loan according to Bankrate’s weekly survey. But what you are offered individually depends heavily on where you apply. Get pre-approvals from your credit union, your primary bank, Capital One Auto Finance, and one online aggregator like myAutoLoan — all within the same 14-day window. Multiple auto loan inquiries within 14 to 45 days count as a single hard inquiry under FICO’s rate shopping protection. This gives you 3 to 5 real rate offers with only one inquiry’s worth of score impact.

Negotiate the Car Price and Financing Separately

Dealers make profit on both the car price and the financing. When they quote a monthly payment, they can hide a high rate inside a seemingly affordable number by extending the term. Always negotiate the purchase price first — get it agreed in writing before discussing financing. Then present your pre-approved rate from your bank or credit union and ask the dealer to beat it. If they cannot, use your pre-approval. This negotiation alone often saves 0.5% to 2% on your rate.

Put Down as Much as You Can — Minimum 10%, Target 20%

A larger down payment reduces your loan-to-value ratio, which reduces lender risk and can improve your rate — especially at near-prime and subprime levels where lender risk tolerance is lower. It also protects you from going upside-down on the loan. On a $25,000 car, the difference between 5% down ($1,250) and 20% down ($5,000) can move you from a 14% rate to a 12% rate at the same credit tier with some lenders — saving over $1,500 in total interest.

Choose the Shortest Term Your Budget Allows

While longer terms (72 to 84 months) have lower monthly payments, they come with higher rates and more total interest. A 48 or 60-month term is usually the sweet spot. A 72-month or 84-month term on a depreciating asset is a recipe for long-term negative equity and high total cost. Compare the total cost — not just monthly payment — for 48, 60, and 72-month terms before deciding. The $40 to $80 monthly difference between 60 and 48 months typically saves $1,000 to $2,000 in total interest.

How to Improve Your Credit Score Before Buying a Car

If your credit score would land you a high interest rate, it might be worth waiting a few months to improve it. Even a 30 to 50 point increase can move you into a better rate tier. Focus on paying down credit utilization by reducing credit card balances, making all payments on time, and disputing any errors on your credit report.

The three fastest credit score improvements before a car loan application are:

- Pay down credit card balances to below 30% utilization — can raise your score 15 to 40 points within one billing cycle (30 to 45 days)

- Dispute credit report errors — a successful dispute can add 20 to 50 points within 30 to 60 days at no cost

- Avoid all new credit applications for 60 days before applying — prevents hard inquiry score drops right before your auto loan pull

The 90-Day Car Buying Credit Strategy

If you need a car in 90 days: Month 1 — pull your credit reports and dispute all errors immediately; pay down any credit cards above 30% utilization. Month 2 — check your updated scores; make all payments on time; stop all new credit applications. Month 3 — get your pre-approvals from multiple lenders within a 14-day window; shop and buy. This 90-day sequence can realistically move you 20 to 60 points, potentially jumping one full credit tier and saving $2,000 to $5,000 on your car loan.

See How Paying Down Balances Would Move Your Score

Use our free Credit Score Impact Simulator to see the estimated point impact of paying down your credit cards before applying for a car loan — and whether it is worth waiting a few months.

Frequently Asked Questions

What credit score do you need for a car loan in 2026?

There is no universal minimum credit score for an auto loan. Most lenders will work with scores as low as 500, though rates at that level are 18% to 25% or higher. For prime rates and the best terms, you generally need a score of 660 or higher. Scores between 601 and 660 fall into the near-prime category and still qualify at most lenders, but with higher rates. For the absolute best rates including 0% APR manufacturer deals, aim for 781 or higher.

What is the current average auto loan rate in 2026?

The current auto loan interest rate sits at 6.98% for a 60-month new car loan, according to Bankrate’s weekly survey updated June 3, 2026. According to Experian, the average auto loan interest rate in the fourth quarter of 2025 was 6.37% for new cars and 11.26% for used cars. These are weighted averages across all credit tiers — your actual rate depends heavily on your specific credit score.

Can I get a car loan with a 600 credit score?

Yes. A 600 credit score sits right at the boundary between near prime and subprime. Where exactly you fall depends on the specific lender’s tier definitions, but in practical terms, you are in a range where approval is possible, but rates will be higher than average, and not every lender will work with you. Credit unions, Capital One Auto Finance, and myAutoLoan are your best options at 600 in 2026.

Does getting pre-approved for a car loan hurt my credit?

Multiple auto loan pre-approval inquiries within a 14 to 45-day window are treated as a single hard inquiry by FICO scoring models. This is called rate shopping protection and is specifically designed to allow consumers to comparison shop without being penalized. Getting pre-approved from 3 to 5 lenders within the same 2-week period results in only one inquiry’s worth of score impact — typically 5 to 10 points — not multiple separate hits.

Is it better to finance through a dealer or a bank for bad credit?

For borrowers with credit below 620, banks and credit unions still typically offer better rates than dealer financing — even for subprime borrowers. Always get a pre-approval from an outside lender before going to the dealership. The dealership may choose to beat your rate to keep the financing revenue in-house, or they may offer the only subprime financing option available in your area. Having a pre-approval gives you a rate benchmark and negotiating power either way.

How much does my credit score affect my car payment?

A borrower with excellent credit will pay around $160 less per month than a borrower with poor credit — and may end up saving over $9,500 in interest over the life of the loan. On a $25,000 loan over 60 months, our analysis shows the difference between a 5.5% super-prime rate and a 16.0% subprime rate is $128 per month and $7,680 in total interest — equivalent to paying $7,680 extra for the same car simply due to credit score.

What is the minimum credit score for 0% APR car financing?

Zero percent APR financing from manufacturers is typically reserved for super-prime borrowers with scores of 720 to 740 and above. These promotional offers are widely advertised but the fine print shows they are limited to buyers with excellent credit, and the 0% offer is usually limited to specific models and shorter terms (24 to 36 months). At 0% APR on a $30,000 vehicle over 60 months versus the current average of 6.98%, you save approximately $5,550 in interest.

Related Free Tools

Related Guides

- Bankrate — Auto Loan Rates, June 3, 2026

- Yahoo Finance — Average Auto Loan Interest Rates by Credit Score, April 2026

- LendBuzz — 600 Credit Score Car Loan: Rates and Approval Odds, April 2026

- Firstcard — Auto Loan Credit Score Requirements 2026, April 2026

- US News Cars — Average Auto Loan Rates, June 2026

- CNBC Select — Average Car Loan Interest Rates by Credit Score, 2026

- Upstart — Car Loan Interest Rate Guide 2026, March 2026

- Experian — State of the Automotive Finance Market Report, Q4 2025

- Federal Reserve — Federal Funds Target Rate, 2026