Best Debt Consolidation Loans for Fair Credit in 2026 — Compare Lenders, Rates, and Real Savings

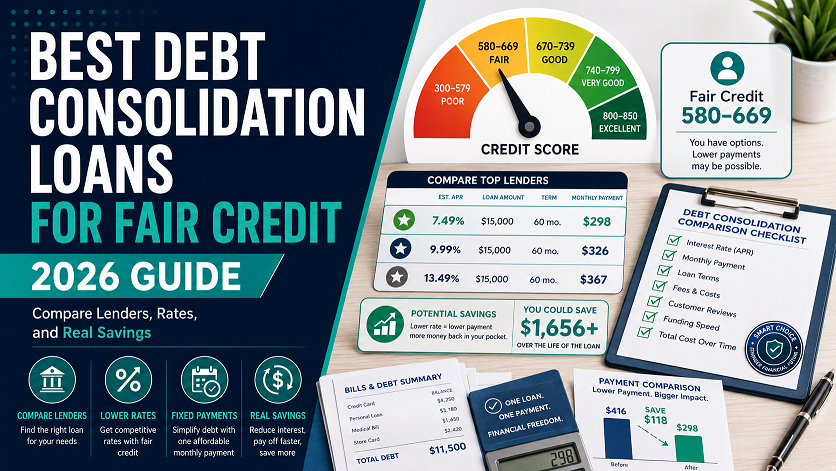

The best debt consolidation loans for fair credit (580–669) in 2026 come from Achieve (min. 620, APR 5.99%–29.99%), Upgrade (min. 600, APR 7.74%–35.99%), Avant (min. 550–580, APR 9.95%–35.99%), and LendingPoint (min. 580, APR 7.99%–35.99%). The average credit card rate is 22% in 2026 per the Federal Reserve. The average consolidation loan rate is 11.65% overall — even at fair-credit rates of 18%–22%, consolidation makes financial sense if you are carrying high-rate card debt. This guide shows you the exact savings math and how to get approved.

If you have fair credit and a stack of high-interest credit card balances, debt consolidation is one of the most financially powerful moves available to you in 2026. The average credit card interest rate in 2026 is 22% according to the Federal Reserve. Meanwhile, as of early 2026, the average personal loan rate for debt consolidation is 11.65%, compared to the average credit card rate of 20.97%.

Even at fair-credit rates of 18%–25%, a consolidation loan can save you thousands of dollars and shave years off your debt payoff timeline — while also simplifying multiple monthly payments into one fixed payment with a clear end date.

The challenge at fair credit is finding the right lender. Traditional banks typically require 660–700+ for consolidation loans. This guide focuses exclusively on lenders that work with 580–669 scores, with real 2026 rate data and a clear savings analysis for your specific situation.

Does Debt Consolidation Make Sense for Fair Credit?

The answer depends on one calculation: is the APR on your consolidation loan lower than the weighted average APR of your current debts? If yes — consolidation saves you money. If not — it does not.

Fair credit borrowers in the 620 to 659 range can still qualify for debt consolidation loans, but rates will likely be higher than for good or excellent credit borrowers. Here is the honest breakdown of when consolidation works and when it does not for fair-credit borrowers:

| Your Situation | Consolidation Makes Sense? | Why |

|---|---|---|

| Multiple credit cards at 22%–29% APR | ✅ Yes | Consolidation loan at 18%–22% saves meaningful interest even at fair-credit rates |

| Credit cards at 20%–22% APR, consolidation offer at 25%+ | ⚠️ Careful | Higher consolidation rate does not save interest — only simplifies payments. May still be worth it for structure. |

| Payday loans at 300%+ APR | ✅ Absolutely | Any consolidation loan under 36% APR is dramatically better than payday debt |

| Medical debt collections at 0% but hurting score | ❌ No | No interest = no savings. Better to pay directly or dispute under 2026 medical debt rules |

| One large low-rate card balance | ❌ Usually not | If your current rate is competitive, replacing it with a fair-credit consolidation rate costs more |

| Multiple debts causing missed payments due to complexity | ✅ Yes — for behavior | Even if rate is similar, one payment prevents late fees and score damage from missed due dates |

How to Calculate Your Weighted Average APR

Add up all your debt balances. For each balance, multiply it by its APR and divide by your total balance. For example: $5,000 at 24% + $3,000 at 22% + $2,000 at 29% = total $10,000. Weighted average = (5,000×0.24 + 3,000×0.22 + 2,000×0.29) / 10,000 = (1,200 + 660 + 580) / 10,000 = 24.4%. Any consolidation loan under 24.4% saves you money on this example debt load.

The Real Savings — What the Numbers Actually Show

The potential savings from debt consolidation depend on your balance, repayment term, and most importantly, the difference between your current interest rate and your new one. Here is the exact math at real 2026 rates:

23% avg APR

Payoff: 11+ years

Total interest: $17,240

22% APR (fair credit rate)

Payoff: 36 months fixed

Total interest: $4,290

The Minimum Payment Trap Is the Real Villain

If you have $11,000 in credit card debt at average rates, paying only minimums will cost you $19,140 in interest on top of the original debt. But if you pay off that credit card debt using an $11,000 debt consolidation loan at 12% APR, you save over $13,000 in interest. The consolidation loan forces you into a fixed payoff schedule — eliminating the open-ended minimum payment spiral that keeps credit card debt alive for decades.

See Your Exact Debt Payoff Savings

Use our free Debt Payoff Calculator — enter your current debts, balances, and rates to see exactly how much consolidation would save you and when you would be debt-free.

Best Lenders for Fair Credit Debt Consolidation in 2026

The best personal loans for fair credit come from Upstart, Avant, Prosper, Best Egg, Upgrade, LendingClub, Achieve, Happy Money, and LendingPoint. Here is the full breakdown of the top lenders specifically for fair-credit debt consolidation:

- Lowest starting APR for fair credit at 5.99%

- Direct creditor payoff available — sends funds straight to your card companies

- Rate discount for co-borrower or proof of retirement savings

- Rate discount when 85%+ of loan funds paid directly to creditors

- 620 minimum — accessible to most fair-credit borrowers

- Minimum loan is $7,500 — not for small debt amounts

- Origination fee 1.99%–8.99%

- Not available in all states — check availability

- At 620 score, actual APR likely 20%–29%, not 5.99%

- Bankrate Best Overall debt consolidation loan April 2026

- Autopay discount lowers your rate

- Direct creditor payoff discount — sends funds straight to cards

- Joint loan option — co-borrower can lower your rate

- Widest loan range: $1,000–$50,000

- Reports to all three credit bureaus

- Origination fee 1.85%–9.99% deducted from loan proceeds

- 600 minimum — 580-score borrowers need to try Avant or Upstart

- Maximum APR 35.99% is among the highest

- Most accessible for 580 scores — lowest minimum of named lenders

- Loans approved in minutes, funds next business day

- No prepayment penalty — pay off early and save interest

- Mobile app with easy payment management

- Hardship program if you face financial difficulties during repayment

- Administration fee up to 9.99% — adds to total loan cost

- No direct creditor payoff option

- Not available in Iowa, West Virginia, Colorado

- At 580, APR likely in the 25%–35% range

- 580 minimum — designed for 580–700 range

- Same-day funding available

- Proprietary scoring considers full financial picture

- Flexible terms up to 72 months

- Soft-pull pre-qualification available

- Origination fee up to 10%

- Not available in Nevada or West Virginia

- Minimum income requirements apply

- No minimum credit score — most accessible of all lenders

- Considers education and employment — not score alone

- Loans up to $75,000 — highest of any fair-credit lender

- Fast approval — often instant decision

- No prepayment penalty

- Origination fee 0%–12% — wide range, can be high

- Only 3-year or 5-year terms — no other options

- No co-signer or joint loan option

- At low scores, actual APR near maximum 35.99%

Side-by-Side Lender Comparison Table

| Lender | Min. Score | APR Range | Loan Amount | Best Feature | Direct Payoff |

|---|---|---|---|---|---|

| Achieve | 620 | 5.99%–29.99% | $7,500–$40,000 | Lowest starting APR for fair credit | ✅ Yes |

| Upgrade | 600 | 7.74%–35.99% | $1,000–$50,000 | Multiple rate discounts available | ✅ Yes |

| Avant | 550–580 | 9.95%–35.99% | $2,000–$35,000 | Best for 580 scores, next-day funding | ❌ No |

| LendingPoint | 580 | 7.99%–35.99% | $2,000–$36,500 | Same-day funding, 72-month terms | ❌ No |

| Upstart | None | 6.70%–35.99% | $1,000–$75,000 | AI underwriting, no score minimum | ✅ Yes |

| LendingClub | 600 | 6.53%–35.99% | $1,000–$40,000 | Peer-to-peer model, direct payoff | ✅ Yes |

| Best Egg | 600 | 7.99%–35.99% | $2,000–$50,000 | Fast approval, secured loan option | ⚠️ Partial |

How Debt Consolidation Affects Your Credit Score

One of the most common questions about consolidation is whether it will hurt your credit score. The short answer: short-term small dip, long-term significant improvement. Here is exactly what happens at each stage:

| Stage | What Happens | Score Impact | Timeline |

|---|---|---|---|

| Pre-qualification | Soft credit pull — no impact | Zero impact | Immediate |

| Formal application | Hard inquiry triggered | -5 to -10 points | Immediate — fades in 12 months |

| Loan opened | New account lowers average account age | -3 to -8 points temporary | First 1–3 months |

| Credit cards paid off | Utilization ratio drops dramatically | +20 to +60 points | 30–45 days after cards paid |

| On-time loan payments | Payment history builds positively | +5 to +15 points per 6 months | Ongoing — builds over time |

| Credit mix improvement | Adding installment loan to revolving mix | +5 to +15 points | Within 30–60 days |

Critical: Do Not Close Your Paid-Off Credit Cards

After using a consolidation loan to pay off your credit cards, do not close those accounts. Closing them eliminates your available credit, which raises your utilization ratio and shortens your average account age — both of which hurt your score. Keep the cards open with a zero balance. If you are worried about overspending, cut up the physical card or freeze it. The account should remain open on your credit report to preserve the credit history and available credit limit.

Alternatives to a Consolidation Loan for Fair Credit

A consolidation loan is not the only option for tackling high-interest debt at fair credit. Here are the main alternatives and when each makes sense:

| Alternative | How It Works | Best Credit Score | Main Advantage | Main Risk |

|---|---|---|---|---|

| Balance transfer card | Move debt to 0% intro APR card — typically 15–21 months | 640–680+ | 0% interest during promo period | Reverts to 25%+ after promo; transfer fee 3%–5% |

| HELOC / home equity loan | Borrow against home equity at secured rates | 620+, homeowner | Rates 7%–9% — much lower than unsecured | Home is collateral — default risk is foreclosure |

| Nonprofit credit counseling / DMP | Nonprofit negotiates lower rates; you make one payment to them | Any score | No loan needed; rates reduced to 6%–8% | Takes 3–5 years; cannot use credit cards during |

| Debt snowball/avalanche (DIY) | Pay off debts in strategic order using extra monthly budget | Any score | No new debt, no fees, builds discipline | Requires strict budget adherence; no rate reduction |

| Debt settlement | Negotiate to pay less than full amount owed | Any — but damages score | Can reduce total owed | -75 to -150 point score damage; taxable forgiven debt |

Nonprofit Credit Counseling — The Underused Option for Fair Credit

If your credit score is too low for a consolidation loan, or if your interest rate offers are not competitive enough to make a loan worthwhile, a Debt Management Plan (DMP) through a nonprofit credit counseling agency is often the best alternative. The National Foundation for Credit Counseling (NFCC) — reachable at nfcc.org — can negotiate your credit card rates down to 6%–8% regardless of your current APR, and you make one monthly payment to them. There is no credit check, no new loan, and it costs approximately $25–$40 per month in fees. The downside is that it takes 3 to 5 years and you cannot use your credit cards during the plan.

How to Qualify for a Debt Consolidation Loan with Fair Credit — Step-by-Step

Calculate Your Weighted Average APR First

Before applying anywhere, calculate your current weighted average APR across all debts you plan to consolidate. Use the formula in Section 1. This is your benchmark — any consolidation loan APR below this number saves you money. Any APR above it means consolidation only helps with simplicity, not cost. This calculation determines whether consolidation is financially justified for you right now.

Check Your Credit Reports for Errors

A single error — a paid collection still showing as unpaid, an incorrect balance, or a late payment that should not be there — can be suppressing your score by 20 to 50 points. Pull your free reports from all three bureaus at AnnualCreditReport.com. Under 2026 medical debt rules, paid medical collections and unpaid medical debts under $500 should already be removed. Dispute anything inaccurate before applying. Moving from 600 to 620 opens Achieve’s program. Moving from 580 to 600 opens Upgrade.

Pre-Qualify with at Least 3 to 5 Lenders Using Soft Pulls

Every major lender on this list — Achieve, Upgrade, Avant, LendingPoint, Upstart — offers soft-pull pre-qualification that shows you real personalized APR offers without any credit score impact. This step is non-negotiable. APRs vary enormously across lenders at the same credit score. One lender may offer 22% while another offers 28% to the same 610-score borrower. Spend 20 minutes pre-qualifying across all five before submitting a single formal application.

Compare Total Cost — Not Just APR

Origination fees can significantly distort APR comparisons. A loan with a 20% APR and a 8% origination fee costs more than a 22% APR loan with no origination fee for shorter loan terms. Always calculate the total dollar cost: principal plus all fees plus total interest over the full term. Divide your loan offer by this total to understand the true cost. Your lender is required by the Truth in Lending Act to disclose the total cost in writing before you sign.

Choose Direct Creditor Payoff If Available

Achieve, Upgrade, Upstart, and LendingClub offer direct creditor payoff — the lender sends funds directly to your credit card companies instead of to your bank account. This option has two major advantages: it often qualifies you for a rate discount (notably at Achieve and Upgrade), and it guarantees the debt is actually paid off rather than potentially spent elsewhere. If direct payoff is available at your chosen lender, always select it.

Keep Your Paid-Off Cards Open and Set Up Autopay on Your Loan

After consolidating, keep all paid-off credit card accounts open with zero balances — this preserves your available credit and improves your utilization ratio. Immediately set up autopay on your new consolidation loan for the full monthly payment — not just the minimum. Autopay also qualifies you for rate discounts at Upgrade and several other lenders. A single missed payment on your consolidation loan would erase much of the credit benefit you just gained.

5 Mistakes to Avoid When Consolidating Fair Credit Debt

Mistake 1: Accepting the first offer without shopping. The spread between the best and worst APR offers for a 620-score borrower can be 8 to 12 percentage points. Pre-qualifying with multiple lenders takes less than 30 minutes and can save thousands. Never accept the first offer you receive.

Mistake 2: Consolidating and then running up new card balances. Paying off your credit cards with a consolidation loan and then charging them back up is one of the most damaging financial mistakes possible. You end up with both the consolidation loan balance and new card debt — double the problem. If you consolidate, immediately drop your credit card spending to essential purchases only until the consolidation loan is paid off.

Mistake 3: Choosing the longest term without running the numbers. A 60-month term on a consolidation loan gives you lower monthly payments but significantly more total interest than a 36-month term. At 22% APR on $15,000: 36 months costs $4,420 in interest; 60 months costs $7,620. The extra $200/month for the shorter term saves $3,200. Always compare total cost, not just monthly payment.

Mistake 4: Not factoring in origination fees. A 10% origination fee on a $15,000 loan means you receive $13,500 but owe $15,000 from day one. If you needed $15,000 to pay off your debts, you may need to borrow $16,700 to net $15,000 after the fee. Always request the net loan amount after fees before deciding if the loan covers your debt payoff needs.

Mistake 5: Closing old credit cards after paying them off. As covered above, closing accounts eliminates available credit and shortens account age — both of which lower your credit score. The goal of consolidation is to improve your financial position, and part of that improvement comes from the score boost of lower utilization. Keep accounts open, use them occasionally for small purchases, and pay in full each month.

Estimate How Much Faster Your Score Improves After Consolidation

Use our free Credit Score Impact Simulator — select “Pay off a credit card” and see the estimated score boost from reducing your utilization after consolidation.

Frequently Asked Questions

What credit score do you need for a debt consolidation loan?

Most debt consolidation lenders require a minimum credit score of 580 to 640. Achieve accepts 620, Upgrade accepts 600, Avant accepts 550 to 580, and Upstart has no minimum. While requirements vary by lender, higher credit scores generally lead to lower APRs and better repayment terms. For the best consolidation rates — below 12% APR — you generally need 700 or higher. At fair credit of 580 to 669, expect APRs of 18% to 30%.

Does debt consolidation hurt your credit score?

Short term, consolidation causes a small score dip — typically 5 to 15 points total from the hard inquiry and new account. Long term, it almost always helps your credit score significantly because paying off credit cards dramatically reduces your credit utilization ratio — the second most important factor in your FICO score at 30%. Most borrowers see a net score improvement of 20 to 50 points within 3 to 6 months of consolidating, assuming they keep their paid-off card accounts open.

Is it worth consolidating debt with fair credit?

Yes, for most fair-credit borrowers who are carrying high-rate credit card debt. The average credit card interest rate in 2026 is 22% according to the Federal Reserve. If you can qualify for a consolidation loan at 18% to 22% — typical for fair credit scores of 620 to 659 — you save on interest, gain a fixed payoff date, and simplify multiple payments into one. The key test: calculate your weighted average card APR and compare it to consolidation offers. If the consolidation rate is lower, consolidate.

What is the average personal loan rate for debt consolidation in 2026?

As of early 2026, the average personal loan rate for debt consolidation is 11.65%, compared to the average credit card rate of 20.97%. As of April 2026, the average rate on a personal loan is 12.27%. These averages are heavily weighted toward prime borrowers. Fair-credit borrowers with scores of 580 to 669 should expect consolidation loan APRs of 18% to 30% from the lenders listed in this guide.

What is the difference between debt consolidation and debt settlement?

Debt consolidation combines your debts into a new loan — you pay the full amount, just at a lower rate with one payment. Your credit score is temporarily dipped then significantly improved. Debt settlement involves negotiating with creditors to accept less than the full amount owed. It severely damages your credit score by 75 to 150 points, and the forgiven debt may be taxable as income. For anyone who can still make payments, consolidation is almost always the better choice. Settlement is a genuine last resort before bankruptcy.

Can I consolidate debt with a 600 credit score?

Yes. Upgrade accepts 600, LendingPoint accepts 580, Avant accepts 550, and Upstart has no minimum. With a 600 score you have solid options at multiple reputable lenders. Expect APRs in the 20% to 32% range. Your income, employment stability, and DTI matter significantly at this level. Pre-qualifying with soft pulls at Upgrade, Achieve, Avant, and Upstart takes under 30 minutes and shows you real personalized offers without any score impact.

How long does it take to get a debt consolidation loan?

Most online lenders fund within 1 to 3 business days after approval. LendingPoint offers same-day funding. Avant typically funds the next business day. If you choose direct creditor payoff — where the lender sends funds directly to your credit card companies — allow 3 to 5 business days for the process to complete. Have your documents ready before applying: two recent pay stubs, a government-issued ID, and your most recent tax return or W-2.

Related Free Tools

Related Guides

- ConsumerAffairs — Best Debt Consolidation Loan Companies 2026, June 2026

- Money.com — 5 Best Debt Consolidation Loans of June 2026

- NerdWallet — Best Debt Consolidation Loans of June 2026

- Bankrate — Best Debt Consolidation Loans, April 2026

- WalletHub — Best Debt Consolidation Loans of June 2026

- CNBC Select — Best Debt Consolidation Loans for Bad Credit, June 2026

- CBS News — How Much Can You Save With Debt Consolidation in 2026, March 2026

- Experian — Best Debt Consolidation Loans 2026

- Bankrate — Debt Consolidation Calculator, April 2026

- Federal Reserve — Average Credit Card Interest Rate 2026

- LendingTree — Best Personal Loans for Fair Credit, June 2026

1 thought on “Best Debt Consolidation Loans for Fair Credit in 2026 — Compare Lenders, Rates, and Real Savings”