Understanding Experian Good Credit Score Range: A Complete Guide for Americans

Updated: June 6, 2026 | Read Time: 13 minutes

You check your score on Experian.com. It says 682. “Good,” it tells you. You apply for a mortgage and get quoted 7.1%. Your friend with a 742 gets 6.3%. Same house, $64,800 difference over 30 years.

So what does “Good” actually mean on Experian? And is it good enough for your financial future in 2026?

Experian is one of the 3 major credit bureaus, and it’s the one most credit card issuers pull for approvals. But “Experian score” can mean FICO Score 8, FICO Score 10T, VantageScore 3.0, or VantageScore 4.0. Each has different ranges.

This guide breaks down exactly what counts as a good Experian credit score in 2026, how lenders really view it, and what you need to do to move from “Good” to “Very Good” where the real money is saved.

Experian Credit Score Ranges: FICO vs VantageScore in 2026

First problem: When someone says “Experian score,” they might mean 3 different things. Here’s the breakdown for 2026:

1. Experian FICO Score 8 Range – What Lenders Use Most

This is the score 90% of top lenders use for credit cards and personal loans. It’s what you see when you buy your score from Experian.com.

| FICO Score 8 Range | Rating | % of Americans | 2026 Reality |

|---|---|---|---|

| 800-850 | Exceptional | 21% | Best rates. Auto-approval. $0 deposits. |

| 740-799 | Very Good | 25% | Prime rates. No Loan-Level Price Adjustments on mortgages. |

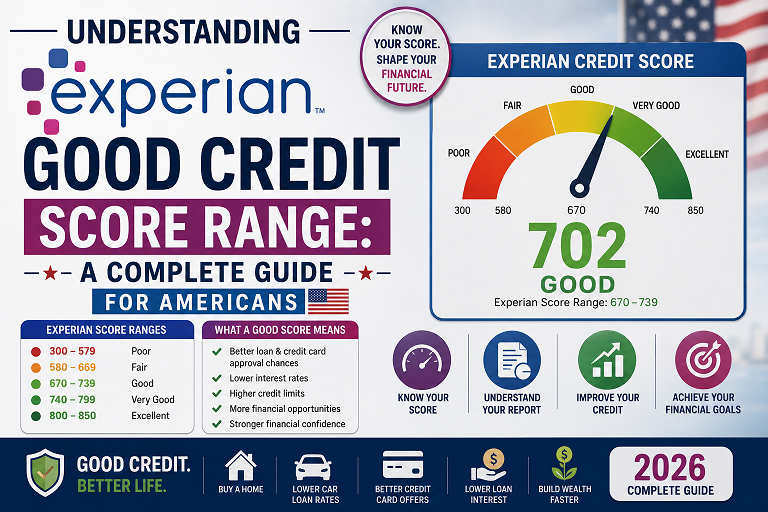

| 670-739 | Good | 21% | Approved for most things. Pay 0.25-0.5% more on mortgages. |

| 580-669 | Fair | 17% | Subprime. High APRs. FHA loans OK, conventional tough. |

| 300-579 | Poor | 16% | Secured cards only. Large deposits. Denials common. |

Key 2026 Insight: “Good” starts at 670, but lenders treat 670 and 739 very differently. A 672 FICO gets 7.15% mortgage rates in June 2026. A 738 gets 6.5%. That’s $47,520 difference on a $400K loan.

2. Experian VantageScore 3.0/4.0 Range – What Credit Karma Shows

If you check Credit Karma, you’re seeing VantageScore 3.0 from Experian and TransUnion. It’s not used for mortgages, but some personal loans and credit cards use it.

| VantageScore 4.0 Range | Rating | How It Compares to FICO 8 |

|---|---|---|

| 781-850 | Excellent | Usually 20-30 points higher than FICO |

| 661-780 | Good | Often 10-20 points higher than FICO |

| 601-660 | Fair | Can be 30 points higher or lower than FICO |

| 300-600 | Poor | Similar to FICO |

Why this matters: You might see 710 VantageScore on Credit Karma and think you’re “Good.” But your FICO 8 could be 682 — “Good” but borderline. Lenders use FICO, not VantageScore, for big loans.

3. Experian FICO Score 10T Range – The New Mortgage Score

FICO 10T rolled out in 2025 and 60% of mortgage lenders use it by June 2026. It uses the same 300-850 scale but weighs trended data — your last 24 months of balances.

| FICO 10T Range | Rating | 2026 Mortgage Impact |

|---|---|---|

| 800-850 | Exceptional | Best rates. No LLPA. |

| 740-799 | Very Good | No LLPA. Prime rates. |

| 680-739 | Good | LLPA starts at 720. Pay 0.25-1.0% more. |

| 620-679 | Fair | Subprime pricing. High LLPAs. |

| 300-619 | Poor | FHA only. 10% down required. |

2026 Change: FICO 10T punishes rising balances harder than FICO 8. If your balances went from $2K to $6K over 24 months, your 10T could be 40 points lower than your FICO 8 even with on-time payments.

External Resource: See official ranges at Experian’s score guide and myFICO.

Is 700 a Good Experian Credit Score in 2026? Here’s What It Gets You

Yes, 700 is “Good” on Experian FICO 8. But “Good” is a wide band. Here’s what 700 actually qualifies you for in June 2026:

What You CAN Get With 700 Experian FICO

| Product | Approval Odds | Rate/Terms at 700 | Vs 760 Score |

|---|---|---|---|

| Conventional Mortgage | 85% | 6.75% with 0.5% LLPA | 760 gets 6.25% no LLPA. Saves $47K |

| FHA Loan | 95% | 6.5% with MIP | Same rate, but MIP cheaper at 760 |

| New Car Loan 60 mo | 90% | 6.9% APR | 760 gets 5.1%. Saves $2,100 |

| Amex Gold Card | 70% | Approved if income $60K+ | 760 gets instant approval, higher limit |

| Chase Sapphire Preferred | 65% | Approved if under 5/24 | 760 gets auto-approval |

| Apartment Rental | 90% | No deposit usually | Same |

| Car Insurance | 100% | Baseline rate | 760 gets 12% discount |

The 700 Problem: You’re approved, but you pay the “Good tax.” Lenders call it risk-based pricing. You get the loan, but 0.25-0.75% higher than “Very Good” tier. That’s $15K-$45K on a mortgage.

The Magic Number: 740

For FICO 8, 740 is where “Very Good” starts. For mortgages, 740 is where Loan-Level Price Adjustments disappear. For auto loans, 740 is “Super Prime.”

2026 Data: Moving from 700 to 740 saves the average American $18,400 over 7 years across mortgage, auto, and cards. That’s a year of college or 20% down payment.

Why Your Experian Score Is Different From Equifax and TransUnion

You check Experian: 712. Equifax: 688. TransUnion: 705. Why? You have three FICO scores, not one.

4 Reasons Experian Differs in 2026

- Not all lenders report to all 3: Your credit union auto loan might only report to Experian. Your store card only to TransUnion. In 2026, 87% of accounts report to all 3, but that 13% gap causes score splits.

- Timing of updates: Chase reports to Experian on the 5th, Equifax on the 12th, TransUnion on the 20th. Pay down a card on the 10th and Experian updates fast, others lag 3 weeks.

- Errors are bureau-specific: Equifax might show a collection Experian deleted. TransUnion might have your limit wrong. 34% of consumers have an error on at least one report.

- Hard inquiry differences: If you applied for a car loan and dealer pulled Experian only, that inquiry drops Experian 5 points but not others.

Which Score Do Lenders Use?

| Loan Type | Which Bureau | Which Score |

|---|---|---|

| Mortgage | All 3 | FICO 2, 4, 5 or 10T. Use middle score. |

| Auto Loan | Usually 1 | FICO Auto Score 8. Often Experian. |

| Credit Cards | Usually 1 | FICO 8. Amex 68% Experian. Chase 52% Experian. |

| Personal Loan | Usually 1 | FICO 8 or 9. VantageScore 4.0 growing. |

| Apartment | Usually 1 | VantageScore 3.0 or FICO 8 |

2026 Strategy: If applying for Amex, optimize Experian. If applying for mortgage, optimize all 3. Pull free reports weekly at AnnualCreditReport.com to compare.

What Impacts Your Experian Score Most in 2026?

Experian FICO 8 uses the same 5 factors as other bureaus, but Experian data has quirks in 2026:

1. Payment History – 35%

One 30-day late drops a 780 to 690. One 90-day late drops 780 to 650. In 2026, BNPL lates from Klarna and Affirm now hit Experian. A $40 missed payment hurts like a credit card late.

Fix it: Autopay everything. Set calendar reminders 5 days before due date. If late, call and ask for goodwill deletion if it’s first time. 40% success rate.

2. Credit Utilization – 30%

This is your balance ÷ limit. Experian updates when lenders report, usually statement closing date. Keep it under 10% for best scores.

2026 FICO 10T twist: Trended data matters. If your utilization was 80% 6 months ago and 10% now, you score higher than someone at 10% flat for 6 months. Paying down debt helps more than low usage alone.

Hack: Pay before statement closes. If limit is $1,000, charge $500, pay $480 before statement, let $20 report. Utilization shows 2%, not 50%.

3. Length of Credit History – 15%

Average age of accounts. Closing your oldest card kills this. Experian Boost now counts utility payments toward age. 24 months of Netflix adds 2 years age if you’re thin file.

4. Credit Mix – 10%

FICO wants cards + installment loans. If you only have cards, add a credit builder loan from Self or Credit Strong. Reports to Experian. $25/month for 12 months = installment loan.

5. New Credit – 10%

Hard inquiries stay 2 years, impact 12 months. One = -5 points. Six in 12 months = -30 points. Rate shopping for mortgage/auto in 45 days counts as one in FICO 10T.

How to Get From 650 to 700+ on Experian in 2026

Here’s the fastest path based on 2026 data. This works if you have no lates in last 12 months.

Month 1-2: Fix Errors and Utilization

- Pull Experian report free at Experian.com. Dispute any errors via certified mail.

- Pay all cards to 1-9% before statements cut. If $5,000 total limits, get balances under $500.

- Expected gain: +20 to +50 points in 45 days

Month 3-4: Add Positive Data

- Sign up for Experian Boost. Connect bank. Adds phone, utilities, streaming. Average +13 points instantly.

- Become authorized user on parent/spouse card with 10+ years history, under 10% util. Adds age + limit. +20 to +40 points in 60 days.

Month 5-6: Credit Limit Increases

Request CLI from existing cards. Capital One, Discover do soft pulls. Higher limits lower utilization. $500 to $2,000 limit = +15 to +30 points if balance stays same.

Month 7-12: Age and Mix

Don’t apply for new cards. Let age increase. If no installment loan, open Self Credit Builder for $25/month. Adds mix + payment history. +10 to +20 points by month 12.

Real 2026 Timeline: 620 to 710

| Month | Action | Score |

|---|---|---|

| 0 | Start: 3 cards, 65% util, 1 collection | 620 |

| 1 | Pay cards to 8% util | 658 |

| 2 | Experian Boost +$12 | 670 |

| 3 | Dispute collection, deleted | 695 |

| 6 | CLI from $500 to $2,000 | 708 |

| 12 | Age hits 2 years, perfect history | 724 |

What Credit Score Do You Need for Common Goals in 2026?

“Good” is relative. Here’s what Experian FICO 8 you actually need:

| Goal | Min Score | “Good” Score | Best Rates Score |

|---|---|---|---|

| Conventional Mortgage | 620 | 680 | 760+ |

| FHA Loan 3.5% down | 580 | 620 | 720+ |

| New Car 0% APR | 700 | 720 | 780+ |

| Used Car Loan | 600 | 660 | 740+ |

| Amex Gold Card | 670 | 700 | 740+ |

| Chase Sapphire Preferred | 690 | 720 | 760+ |

| Apartment – No Deposit | 650 | 700 | 750+ |

| Car Insurance Best Rate | 700 | 750 | 800+ |

2026 Reality: 670 gets you in the door. 740 saves you money. 800 is bragging rights but doesn’t get better rates than 780.

Frequently Asked Questions

What is a good Experian credit score in 2026?

For Experian FICO Score 8, ‘Good’ is 670-739. ‘Very Good’ is 740-799. ‘Exceptional’ is 800-850. Most mortgage lenders want 740+ for best rates in 2026. Auto lenders consider 700+ good and 661+ prime.

Is Experian FICO score the same as VantageScore?

No. Experian provides both FICO scores and VantageScore 3.0/4.0. They use different models. A 720 FICO can be a 690 VantageScore. Mortgage lenders use FICO. Credit Karma shows VantageScore. Always check which score you’re seeing.

Is 700 a good credit score on Experian?

Yes. 700 is in the ‘Good’ range for Experian FICO 8. You’ll qualify for most credit cards and auto loans. But for mortgages in 2026, 740+ gets you Loan-Level Price Adjustments waived and rates 0.25-0.5% lower.

Why is my Experian score different from Equifax and TransUnion?

Each bureau has different data. Not all lenders report to all 3. Experian might show a collection that Equifax doesn’t, or a credit limit that TransUnion has wrong. Timing of updates also varies by 30-45 days.

Free Tools to Monitor Your Experian Score in 2026

- Experian.com: Free FICO Score 8 updated monthly. Free report and Experian Boost. No credit card needed.

- Discover Credit Scorecard: Free FICO 8 based on Experian, even if not a customer. Updates monthly.

- AnnualCreditReport.com: Free full reports from all 3 bureaus weekly. Use this to dispute errors.

- Bank/Credit Union: Chase, Bank of America, Wells Fargo, and many credit unions give free FICO scores in their apps.

Avoid: Credit Karma shows VantageScore 3.0, not FICO. Useful for monitoring but not for loan applications. Your FICO could be 40 points lower.

The Bottom Line: What’s a Good Experian Score in 2026?

Technically: 670-739 is “Good” per Experian.

Realistically: 740+ is where you want to be. That’s “Very Good” and gets you best rates, no deposits, and instant approvals.

Minimum for goals:

- Mortgage: 620 to qualify, 740 for best rates

- Car loan: 660 for prime, 700 for 0% deals

- Amex Gold: 670 to have a chance, 700+ for good odds

- Apartment: 650 no deposit, 700 preferred

If you’re under 670, focus on utilization and errors first. If you’re 670-739, you’re “Good” but paying the “Good tax.” Push to 740. It’s worth $15K-$85K over your lifetime.

Check your Experian FICO 8 today. Know your number. Then use the steps above to improve it. Your financial future literally depends on it.

Next Reads: 21 Ways to Improve Your Credit Score Fast | Amex Gold Credit Score: What You Need | How to Fix Errors on Your Credit Report