See how different financial actions, like opening a new card or missing a payment, might impact your credit score.

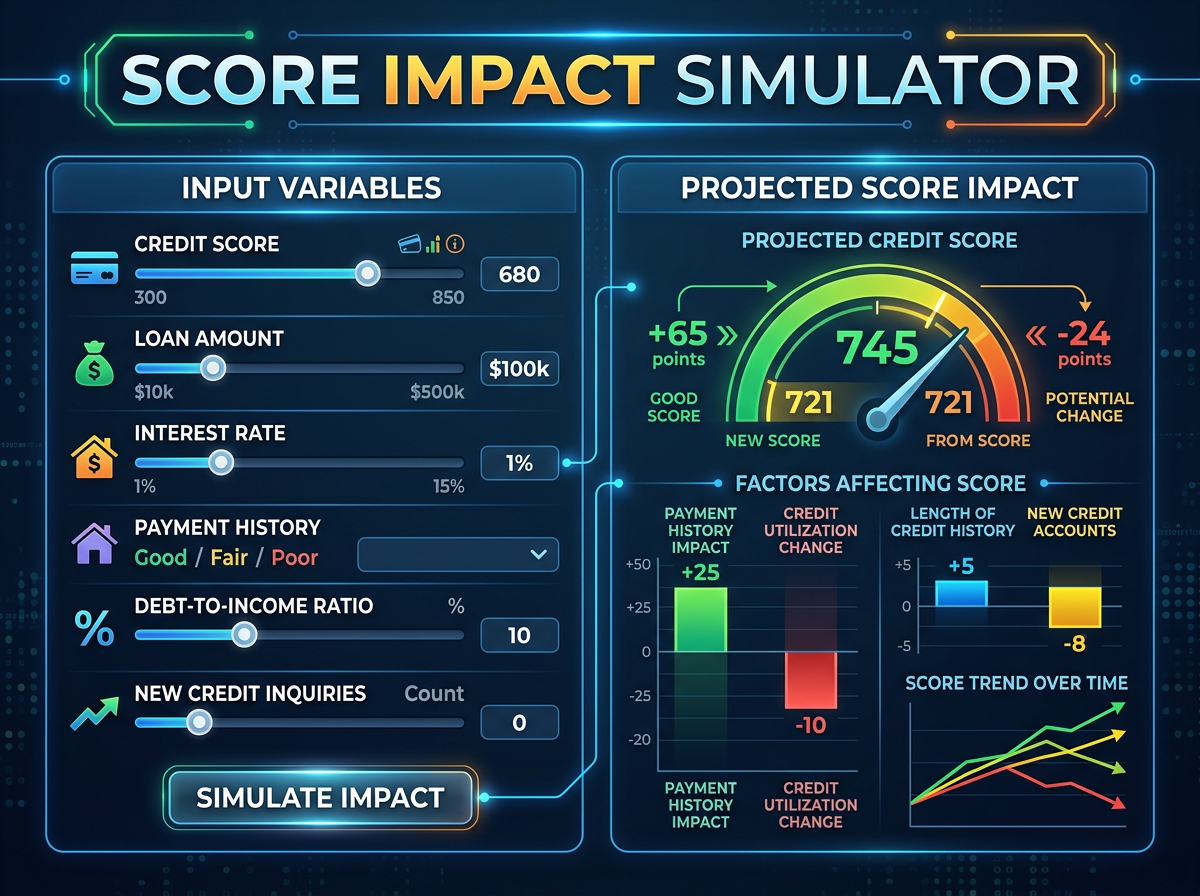

Credit Score Impact Simulator 2026 — See How Any Action Will Affect Your Credit Score Before You Do It

Every credit decision has consequences — some positive, some negative, some both at once. Before you apply for a new credit card, close an old account, or make a large purchase that spikes your utilization, it pays to understand how that action will affect your credit score.

This simulator uses FICO scoring guidelines to estimate the point impact of 12 common credit actions. Select multiple actions to see the combined effect on your score. Use it to plan your credit moves strategically — especially before applying for a mortgage or major loan.

- Enter your current credit score using the slider or input box. Use your actual FICO score if you know it, or use our Credit Score Estimator to get an estimate first.

- Click any action cards to select actions you are considering or have recently taken. You can select multiple actions — the simulator adds the impacts together.

- Read the Before and After scores in the results panel, along with the timeline note explaining how quickly the change would show up on your actual report.

Credit Score Impact Simulator — 2026

What Each Credit Action Actually Does to Your Score

Credit score changes are not random. Every action maps to one or more of the five FICO factors — and understanding exactly which factor is affected tells you how serious the impact is and how long it will last.

| Action | FICO Factor Affected | Typical Impact | How Long It Lasts |

|---|---|---|---|

| Pay off credit card balance | Utilization (30%) | +25 to +50 points | Reverses if balances rise again |

| Miss one payment (30 days late) | Payment history (35%) | -60 to -110 points | 7 years on report; impact fades after 2 |

| Remove a collection account | Payment history (35%) | +30 to +80 points | Permanent improvement |

| Apply for new credit card | New credit (10%) | -5 to -15 points | Inquiry stays 2 years; score recovers in 12 months |

| Close an old credit card | Utilization + History length | -10 to -30 points | Can be permanent if oldest account |

| Open a credit builder loan | Credit mix (10%) | +10 to +25 points | Builds over 6–12 months of payments |

| Become authorized user | Payment history + Utilization | +15 to +40 points | As long as the account remains open |

| File bankruptcy | All factors | -130 to -200 points | 7 years (Ch.13) or 10 years (Ch.7) |

The 3 Most Common Mistakes People Make With Credit Actions

- Closing old accounts before applying for a mortgage — Many people try to “clean up” their credit by closing unused cards before a big application. This is the opposite of what helps. Closing accounts raises your utilization and shortens your credit history — both of which lower your score.

- Applying for multiple credit cards in a short period — Multiple hard inquiries in a short window signal financial stress to lenders. While mortgage and auto loan inquiries within 14 to 45 days are treated as one, credit card applications are not. Space applications at least 6 months apart.

- Paying off an installment loan and expecting a big score jump — Paying off a mortgage or auto loan can cause a small short-term dip because it closes an account and reduces credit mix. The dip is usually small (5 to 10 points) and temporary — do not let this dissuade you from paying off loans.

Frequently Asked Questions

How accurate is this simulator?

This simulator uses standard FICO scoring guidelines and typical point ranges based on published research and credit industry data. It is directionally accurate — it will reliably tell you whether an action helps or hurts, and by roughly how much. However, the exact impact on your score depends on your complete credit profile. People with higher scores often experience larger drops from negative actions. People with lower scores often see larger gains from positive actions.

Why does the same action affect different people differently?

FICO scoring is relative to your existing profile. A missed payment hurts someone with an 800 score more than someone with a 600 score because the 800-score person has more to lose. Similarly, paying off a collection has a bigger impact on someone with no other negative marks than on someone with multiple collections. The simulator shows typical ranges — your actual result may be higher or lower.

Can I recover from a bankruptcy or missed payment?

Yes — both are recoverable with time and consistent positive behavior. A bankruptcy causes severe initial damage, but many people with a bankruptcy on their record reach scores of 650 to 700 within 2 to 3 years by using secured cards responsibly, keeping utilization low, and making every payment on time. A single 30-day late payment, while damaging, typically loses most of its impact after 18 to 24 months of clean payment history.

Ready to take action on your score?

See our complete step-by-step guides for the most impactful credit actions you can take right now.

Read the improvement guide →